The Great Collateral Reset: Fiat Currencies and Bonds > Bitcoin and Gold. Courtesy of Mark Jeftovic at Bombthrower.com

Introduction

This post will bolt on to my previous trilogy, and is an extension to discuss the emerging wars inside the banking system, between private banks and public (central) banks, will go into the history of banking and central banking and their relationship, and the evolution to the Dollar as World Reserve Currency and the Eurodollar Shadowbank World Reserve Currency… While the public narrative from finance, mainstream media, economists and academia places Central Banking as central to national financial systems, the reality is that for the last eight decades the private and international banking system found a workaround for the US Dollar by creating offshore Dollars, aka EuroDollars, a worldwide and intricate ledger entry book-keeping network, that has evolved alongside National Government bond (debt) markets as underlying collateral and balance sheet reserves… This worldwide inter-bank network exploded after the last depegging from gold in 1971 and the Great Inflation of the 1970’s, continuing its meteoric growth and zenith by mid 2007, when something snapped… Since the Great Financial Crisis of 2008 and 2009 the world has suffered from persistent EuroDollar shortages, financial de-risking and stuttering credit and loan creation that some have called the Silent Depression, and has led to the fragmenting of the global trade economy, reflected in increasing poverty, public discontent, Populist and Nationalist breakaway movements such as Brexit and Trump, and the glaring geopolitical fractures between West and East, in competing trading blocks and currencies…

The accelerating trend of de-globalisation and re-shoring of supply chains in energy, industry and manufacturing, will be hugely inflationary for Western currencies and countries, undermining their government bond markets, and necessitating the transition to superior and Proof of Work produced collateral in gold and Bitcoin, that will underpin the balance sheets of central banks, the banking sector and the whole corporate sector, as they are revalued higher… The revaluation of Gold and Bitcoin will come at the cost of devaluing Central Bank and Nation State borrowing and spending power, and is probably the next workaround for the survival of the Eurodollar system, and a re-booting of the world financial system and accounting power structures…

Bitcoin Kills Banking – How it Happens and Why It Will Happen

My initial post on Bitcoin killing Banking was published nearly eight years ago, and boiled down to some very simple plot lines: the financial crisis of 2008 had effectively bankrupted the private banking system, and that central banks through control of the public narrative parroted by the media they employ, had come to the rescue of a system visually imploding, principally by abolishing FASB157 and Mark to Market Accounting, and by driving short term interest rates to zero (ZIRP), and flooding the world with Quantitative Easing, the so-called printing of money… This lowered the debt burden of a debt based system allowing banks, corporations and governments to borrow and finance their debts on the cheap, by penalising producers and savers with the double whammy of debasing fiat currencies and zero interest on saving, and was a massive wealth transfer from the productive sector to the unproductive sector…

However, these accounting tricks and psychological sleights of mind come with trade offs, that of compressing Net Interest Margins via Bond Yield Curves that traditional banks depend upon as collateral for borrowing short and lending long, making banks ever more unprofitable, that would doom them inside this terminal circle of zombie institutions in Dante’s Inferno of usury, which I also described as the mother (central banks) poisoning the children (private banks) in trying to save them since 2008…

In Bitcoin, then trading at a few hundred dollars each, I described a completely different accounting standard to our current moribund banking system, that was decentralised not centralised, open source and transparent not secretive and fraudulent, vibrant and growing not sullen and stagnating, in the eight years since Bitcoin has exploded in price and value, into public consciousness and especially into mainstream financial consciousness which is fuelling everything that is happening today… But fundamentally I described Bitcoin as a competing ledger and currency system against banking and central banking, and a competing system that banks and central banks would increasingly have to pivot into, for banking fees from Bitcoin exchanges, trading fees from Bitcoin markets, and for price appreciation and liquid collateral on balance sheets, if and when the banks signed The Faustian Bargain and the Deal with the Devil, that of regulation and access into the legacy financial system, thus building the bridges to connect two distinct ecosystems, the Fiat ecosystem and the Bitcoin ecosystem… Because the wealth of the world is currently accounted for and contained within the Fiat Ecosystem and their legal tender laws, it would be the banks as incumbents and principle government licencers and lobbyists that would get to decide if they embraced Bitcoin, and all the fees, taxes and tolls they could charge for letting wealth leak and flow from the Fiat Ecosystem into the Bitcoin Ecosystem, thus blowing up the value of Bitcoin while sucking the value out of Fiat…

Bitcoin Kills Banking Revisited

I revisited my original post in June of 2017, with Bitcoin trading at a few thousand, with an update that covered the rise in the “crypto-craze” that had flowed way outside Bitcoin and into Ethereum, Ripple XRP and various other assorted altcoins, as Bitcoin Dominance was decreasing (as it tends to do during risk on bull markets and cycle tops), and with a detailed discussion of game theory in regulation and adoption of Bitcoin by the world’s nation states and their banking systems… Indeed, I pinpointed this continued and more detailed regulation of Bitcoin on a State by State basis as the biggest trend to be watching during 2017 and 2018, and this has only become more important in the six years since… My simple premise lied in the fact that Bitcoin is a single and uniform ledger and currency network operating in all two hundred of the world’s nation states simultaneously, a decentralised and anti-fragile honey badger pitted against centralised and fragmented national banking networks and cartels, and so Bitcoin would eventually divide and conquer each country individually, by regulation and taxation, pitting Nation State against State in their adoption or dis-adoption of Bitcoin…

I predicted in line with game theory that the West would clamp down and more tightly regulate Bitcoin as issuers of the Dollar and Euro and the vast majority of global trade settlement currencies and collateral, and that the countries in the East, as a workaround for the the SWIFT and Dollar and Euro centric trade settlement systems, would regulate Bitcoin more lightly and possibly even embrace it as a transparent and censorship resistant alternative to the increasingly politicised and sanctioning mechanism of SWIFT and EuroDollar hegemony… I also described Bitcoin as a preferable alternative to World War III, as this allowed a controlled demolition of the Dollar based international system, and the gradual adoption of Bitcoin as a mutual and voluntary trade settlement network and currency between Nation States, especially in the event of sanctions and hostility from incumbent Western nations…

The following year in 2017, China “banned” Bitcoin regulated exchanges and in 2021 went full retard in “banning” mining, Bitcoin’s hash rate halved in the month of May 2021 as China effectively went dark, before rebounding as miners relocated and gave a massive boost and subsidy to mining outside of China, especially to the US… Thus it seems that the Chinese Communist Party has forsaken the geopolitical advantages of Bitcoin, in maintaining the iron fist of control over its people, and the promotion of its e-yuan electronic currency, even as we currently see Hong Kong (Chinese controlled) start to position itself as an off shore hub for the re-embrace of Bitcoin… Russia, on the other hand, the victim of direct Western sanctions, in freezing of foreign reserves and cut-off from banking networks, is working toward designating Bitcoin as a foreign currency for international trade, and with cheap Russian electricity already home to 10% of Bitcoin’s global hashrate today, Bitcoin mining and the Russian Government may well become more intertwined in the future….. In the US, it appears there is increasing Government hostility against Bitcoin under the Biden Administration, with the recently reported Operation Chokepoint 2.0 attempting to starve Bitcoin exchanges and crypto banks to cut them off from the traditional bank and finance sector, the EU has recently brought out its MICA regulations to harmonise crypto laws for all its member states (and to mixed reviews), and there is some hype among Venture Capital and crypto companies lately that the UK is positioning itself as a hub for Bitcoin and crypto, of which I’m struggling to see myself…

Outside of the Developed World and its monopoly over world currencies, and in the Developing World, El Salvador became the first country to officially adopt Bitcoin as legal tender alongside the US Dollar on the 7th of September 2021, and the Central African Republic became the second on 27th April 2022… There has also been reporting on the Islands of Tonga and Fiji adopting Bitcoin as legal tender to solve their own foreign currency problems, being dependent on their diaspora populations living abroad to send money home, contributing 11.3% of Fiji’s GDP and a mindbending 45.5% of Tonga’s GDP in 2021, these island states are hostages to the Eurodollar, and Western Union and Moneygram that monopolise international remittances and charge extortionate fees on sending money… There is also Panama where Bitcoin has been clearly regulated and while not strictly legal tender, there are no capital gains taxes on Bitcoin investments which puts Bitcoin on an equal footing with the Panamanian Balboa and the US Dollar, the official currencies… It seems that the drive toward Bitcoin legal tender status is being driven at the peripheries, in poor and underbanked countries at the furthest extermities of the global financial system, where shortages of credit and currencies are at their most acute, and which makes the adoption of Bitcoin most attractive…

Bitcoin Kills Banking Redux: Exchanging and Exchanges

My third post released in February 2019 with Bitcoin then still trading at a few thousand dollars, concentrated more on this question of exchanges, of course subject to National government and banking regulation, which I broadly categorised in the following divisions:

1 Decentralised Exchanges – Non KYC/AML or semi anonymous exchange, which could be face to face or over the internet, through cash or bank transfer, or via ATM’s that are proliferating over the world but especially in the West, as CoinATMRadar lists over 36,000 at present; in short decentralised exchange is peer to peer and generally outside of regulation and therefore taxation… The trade off for this method of exchange is gaining privacy and tax evasion, while sacrificing convenience and liquidity, the price you pay for privacy is a higher margin and a more complex user experience than regulated and liquid exchanges… This method also reflects Bitcoin’s more libertarian and agorist origins, peer to peer and in the real economy, the earliest and most hardcore Bitcoin adopters will sacrifice any and all connections with fiat currencies for transacting and living in the circular Bitcoin economy, and at its most decentralised and anti-fragile extreme… These are also in my opinion the people that will keep Bitcoin honest at its fringe, and in keeping it real will counteract the inevitable financialisation and fiat’s attempts to infiltrate and centralise the Bitcoin network, and the purest and therefore most sustainable Bitcoin economy…

2 Cash Apps – The proliferation of smartphones from 2010 onwards and Bitcoin exchanges from 2011, have converged in the last few years with mobile Bitcoin exchanges, which are rising ubiquitously by the way, from Coinbase Mobile and Block’s Cash App, to Robinhood, Paypal, SwanBitcoin, Relai.ch, PeachBitcoin and many more I can’t think of… These Mobile apps, as should be expected, are especially intuitive and convenient with a corporate User Interface and far more professional and efficient than the Decentralised Exchanges described above, with the trade off of course, of corporate surveillance and particularly close relationships to the banking establishment and compliance they are dependent upon… The price you pay for convenience and the slick corporate interfaces with fiat currency rails is a severe reduction in privacy, which is why few will seek the decentralised method above and outside the system, the vast majority of “normies” are more than willing to sacrifice privacy for convenience, as the popularity of these many apps operating largely over the West attests… And to me these apps despite their privacy defects are a highly effective and user friendly method of getting bitcoin into the hands of the people, and virtually all of these apps allow the physical withdrawal of bitcoin to private cold storage, which also allows them directly into the Bitcoin ecosystem…

3 Centralised Exchanges – Whereas decentralised exchanges and cash apps cater exclusively to retail and the individual, I focused more on the institutional developments that were then happening in the realm of the centralised exchange, and its increasing interaction with what I termed the Wolves of Wall Street… While exchanges were initially lauched for the retail user, from Mt Gox, to Bitstamp, Coinbase, Bitfinex, Kraken, Gemini and others that launched in the early twenty tens, with increasing legislation and clarity around regulating Bitcoin in the US (and outside the US), institutional money and capital from the most financialised country on earth has started searching for avenues into Bitcoin ownership and trading, which should be well known to anyone following this space… The last four years has really been the prelude to my long predicted stampede of family funds, hedge funds, mutual funds, pension funds, insurance funds, any and every other fund seeking to hedge fiat currency destruction with sovereign unadulterated digital collateral…

4 Fiat Derivatives (Cash Settled Futures, ETF’s) – Two sets of cash settled futures heralded the age of derivatives and which top ticked nearly perfectly Bitcoin’s blow off top bull market in late 2017, both out of that commodity trading mecca of Chicago, with the CBOE (Chicago Board of Exchange) and CME (Chicago Mercantile Exchange) launching cash settled futures derivatives… While the CBOE dropped Bitcoin futures in 2018, CME Bitcoin futures are now firmly established which has allowed Wall Street and institutions to have exposure to the Bitcoin price without having to buy bitcoin, and has also allowed a convenient method of shorting Bitcoin, furthermore Bitcoin Futures have also been launched in most Western Countries since… I also discussed ETF’s (Exchange Traded Funds), and while the SEC under Gary Gensler have approved the launches of Bitcoin Futures ETF’s, despite the ongoing efforts of Grayscale, CBOE, VanEck, Bitwise, Ark, Nasdaq, Fidelity, Invesco, Valkyrie, and the latest filing by asset management behemoth Blackrock ramping up further pressure for SEC approval, no spot and physical ETF’s have launched yet in 2023….

5 Banking Protocols – I described altcoins such as Ripple XRP and Stellar Lumens as banking protocols or fintech platforms, sovereign networks and currencies that would allow banks to plug into and interact, and similar to SWIFT could act as interbank networks to streamlime operations and trade settlement, and which had back in 2019 courted some interest from banks at the time… Because of the proximity of Ripple and Stellar Lumens to the crypto exchange space, I also envisioned these banking protocols as frictionless transitionary layers between banking and Bitcoin, if the banks did decide to adopt them…. Four and a half years later, we have seen little progress in this area, and while Ripple have just given the SEC a huge black eye in a multi year lawsuit, it feels safe for me to say that it’s unlikely these protocols will be adopted by the banking system to the scale I imagined in past years, and so I pay far less attention to this exchange prototype space these days…

6 Stablecoins – Stablecoins are a hybrid and legal gray area, transforming exchanges into Banks or Money Market Funds in the creation of what has been described as crypto EuroDollars, in that they are pegged to fiat currencies, practically all of them Dollar denominated, which began with veteran offshore exchange Bitfinex with Tether, that spread to Circle, Coinbase, Gemini, Binance, and even attempted by Facebook with Libra, that bit the dust and was abandoned due to the hostility of US Congress and regulators, fearing competition in the realm of counterfeiting currencies… Indeed, stablecoins like banking protocols have been largely stymied and slowed down in US onshore exchanges, and despite USD Circle having grown to $27 billion at the time of writing, the crown in stablecoin land has long been worn by Bitfinex and has largely been able to skirt the US government and its regulators, with Tether currently issuing over $83 billion in USDT, despite all the doom mongering and FUD since at least 2017… I predicted in 2019 that competing stablecoins issued by rival and more transparent exchanges would chip away at Tether’s dominance of the sector over time, and it has not really aged well so far… Bitfinex and Tether are still around and don’t look to be going anywhere soon, mostly thanks to US regulators who have clamped down on US competition, and this space seems to be stagnating at this point along with banking protocols…

Just as I was losing interest, along comes Paypal, one of the world most recognisable payment processors, with its launch of Paypal USD (PYUSD)… This is huge for the stablecoin space!

Bitcoin Kills Banking Bolt On: Banks vs Central Banks, Eurodollar vs Dollar, and Bitcoin Collateralisation

So having extensively dealt with Bitcoin exchanges in the last post, this post will discuss the other side of the exchange relationship, that is banking and fiat currencies, the incumbent and long established system of fractional inter-bank lending based on collateral, that was spawned during Europe’s unfortunate Reformation… And this post will focus on the divisions within banking, and increasingly between central banks and commercial banks over the collateralisation of gold, sovereign national debt (bonds) and Bitcoin, as the underpinning for the balance sheets and ledger accounting of banks, that is somewhat different from the modern mainstream explanation of how banking and finance operate… For banking is the business of accounting, of assets and liabilities, of balancing sheets and ledger entries, and on hypothecating and rehypothecating collateral in order to create credit and loans, and what is termed in modern clown world as “economic growth”…

The Origin of Banking

Once we have the Origin of Money (Phoenicians, Lydians, or Persians – take your pick) and the mass adoption of a collective trading mechanism, remaining quirks and inefficiencies will eventually be “remedied” by the Origin of Banking, and a second layer solution consisting of ledgers and credit substitutes… As I elaborated in a previous post, double-entry book-keeping technology explodes in the Fourteenth and Fifteenth Centuries, and out of the Northern Italian city states of Venice and Florence… With the birth of the balance sheet, and double entry, i.e assets (debit) and liabilities (credit) allow incomings and outgoings to be monitored without having to transact gold and silver coins or bullion, leather bills of exchange (legal contracts) and paper money (cash) are substituted in exchange between merchants, if not the general public yet… With ledgers and inter-merchant contracts and derivatives combined, we have the origin of merchant banking where gold is effectively collateralised and held as a balance sheet asset, underpinning the burgeoning credit layer and a certain disconnect between the underlying precious metals and the overlying derivatives, leading increasingly to fractional reserve banking, misallocations of capital, usury, and business cycles of boom and bust… The destabilisation of Europe awaits…

The Origin of Central Banking

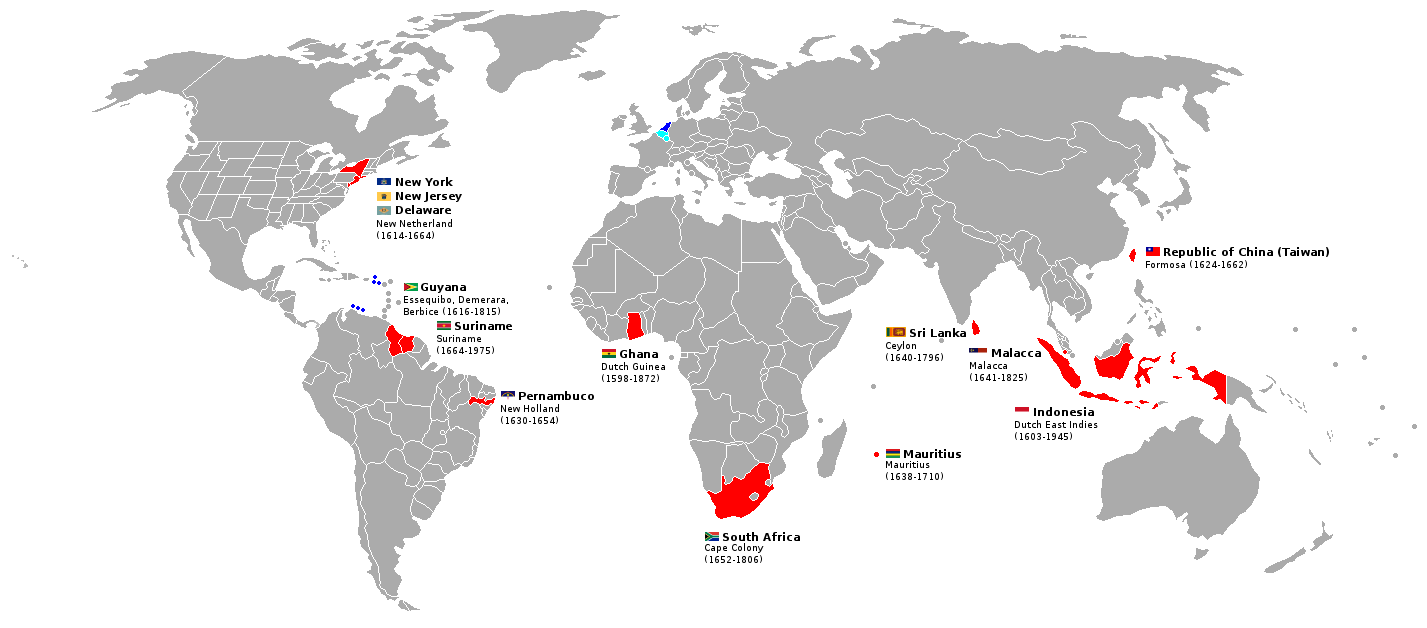

National Banking aka Central Banking is the spawn of the Protestant Reformation, and the radical centralisation of State power usurped by Kings, Princes and Parliaments (Republics), and it should be clear why central banking comes about: bankers and financiers seeking monopolies in the financing of wars and empires, and kings and princes seeking financing from bankers and financiers for expanding wars and empires… The prototypical central bullion bank was the Amsterdamsche Wisselbank founded in 1609, slap bang in the middle of the Dutch Protestant Eighty Year War (1568-1648) against the Spanish Habsburgs, and principally invented as a fully reserved bullion bank to defend the Dutch coinage standard that varied wildly in coins and purities… It would eventually evolve into fractional reserve banking to finance the rather remarkable and undertalked Dutch Empire, especially the Dutch West India and Dutch East India Corporations that ruled global trade for nearly two centuries, indeed the Bank Guilder would become an international and global reserve currency, and a de facto reserve currency for Europe during the Seventeenth and Eighteenth Centuries…

The memory holed Dutch Republic and Empire (source)

The model of the Wisselbank as a state bank was adapted further by newly created Protestant Nation States following the Thirty Years War (1618-1648), that also established Westphalian Sovereignty aka International Law, the first official Central Bank (and still the world’s oldest) being the Sveriges Riksbank of Sweden established in 1668… Twenty years later England and Britain would undergo its own Colour Revolution and a centrally financed state and economy, when the bankers of Amsterdam would finance the Orange Revolution, also known as the Glorious Revolution of 1688, the removal of Catholic James Stuart II/VII and the installation of William III of Orange, and a Protestant Crown… Only six years, Amsterdam’s bullion banking model would be transplanted into the dark square mile of the City of London, with the Old Lady of Threadneedle Street, the Bank of England established in 1694…

The Bank of England and The Rise of The British Empire

The origin of the Bank of England is founded upon war, and the raising of funds for armies and navies to compete with the Dutch and French Empires of the late Seventeenth Century, in ironworks and agriculture that started to transform the domestic economy… In 1707 the Acts of Union were financed largely by the Bank of England by bribing the upper echelons of Scottish society to consolidate a new and larger Customs and Currency Union, while Scotland’s ruinous experiment with colonialism and the Darien Scheme in New Caledonia (Panama) had left the Scottish government largely bankrupt…

The upshot of Union created a far larger Geopolitical power and economy to challenge the might of the Dutch and French Empires during the Eighteenth Century, and while the East India Company had become the Crown’s main trade monopoly in 1600 (under Elizabeth I), the Bank of England would become the (increasingly Parliamentary following the Glorious Revolution and the supine Hanoverian monarchy) British State’s second institution… The South Sea Company did briefly rise in competition with the BofE to reduce the national debt by establishing trade colonies in South America, but the collapse of the South Sea Bubble in 1720 that fleeced and ruined many in the British elite, would cement the Bank of England as Britain’s colonial financier…

At that stage in its history the Bank had little connection with the rest of Britain’s private banking network, but moving through the Eighteenth Century this began to change, and by the 1781 Renewal Charter, the Bank of England was considered the banker’s bank, with BoE banknotes fungible with gold bullion under the blossoming Gold Standard (from 1717), that was usurping silver as the metal of choice by the beginning of the 19th Century by British Mercantilism…

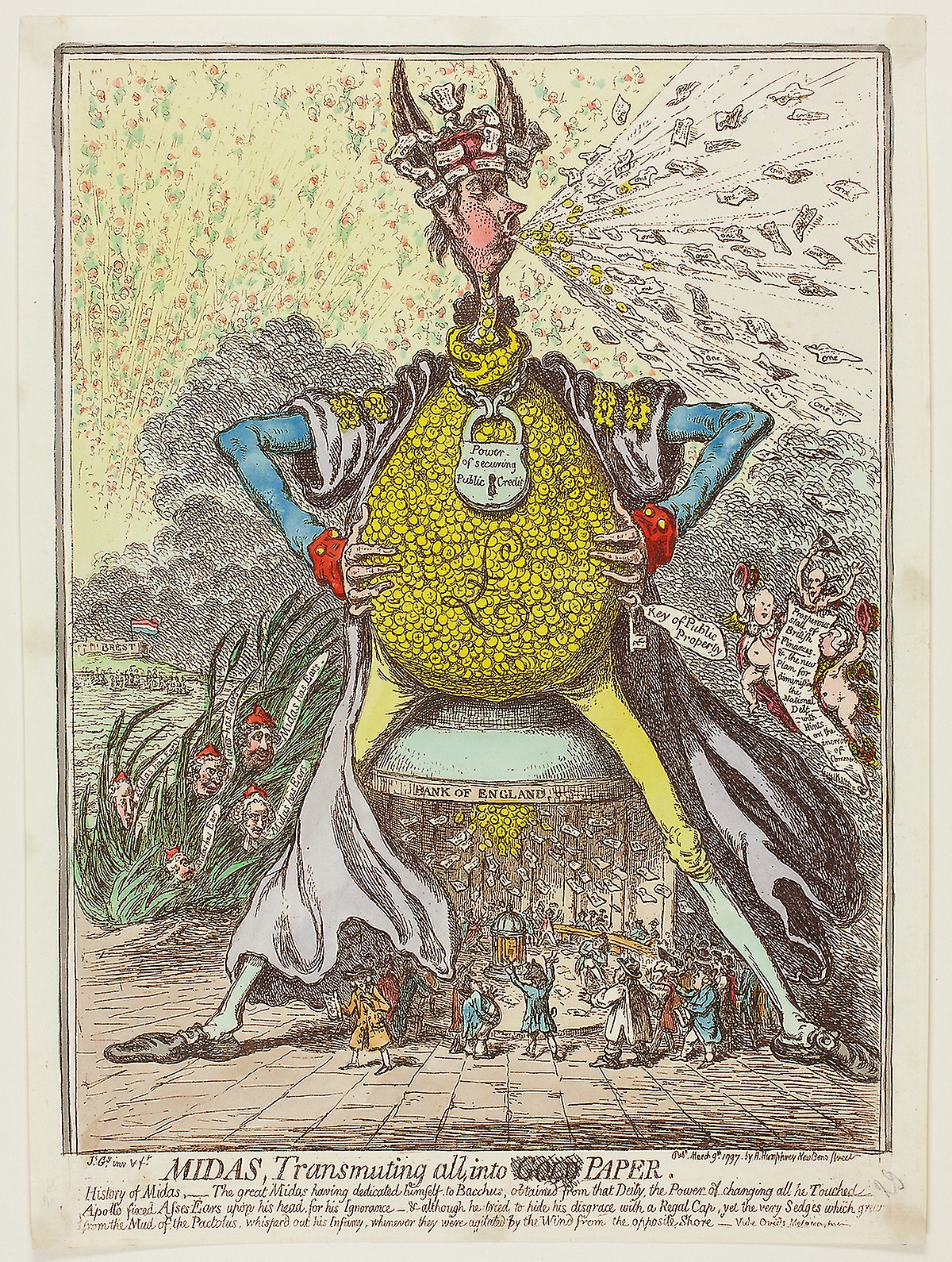

The Bank Restriction Act of 1797

Satirical Cartoonist James Gillray lampooning the criminal syndicate between the British Government and the Bank of England

With the Bank of England acting as the principal bank of the British Government in matters of debt and financing, and also as a central repository of asset swaps for the British private banking network by leveraging gold deposits with issue of paper banknotes, conditions were in place for an epic rug pull that would light a fire under Britain’s population boom and industrial revolution, that would be exported (along with Central Banking) to the rest of the West during the Nineteenth Century, and to the rest of the world during the 20th Century… Having largely defanged the Dutch Empire by 1800, Britain’s major geopolitical rival would be post Bourbon and Catholic France in the midst of its bloody and Republican (Protestant) Revolution (1789-1799), and the British State had since 1793 when William Pitt The Younger declared war on France, been in an arms race built on the Bank of England’s banknotes… This overprinting of banknotes compared to its gold deposits would lead to a bank run triggered in the North East of England in late 1796, and was catalysed by the French Invasion in the Battle of Fishguard in February 1797, with £11 million of banknotes in circulation and only £5.5 million in gold deposits, the Bank of England avoided bankruptcy thanks to the British Government suspending the gold standard within Britain for a period of 24 years, and until May 1st 1821, a generation unchained from gold which would have the greatest of consquences for the future of the world…

Wiki quote for above cartoon: “After the passing of the [Bank Restriction 1797] act, Richard Brinsley Sheridan publicly bemoaned the way in which the Bank of England had fallen under the influence of William Pitt the Younger by describing the institution as “An elderly lady in the City, of great credit and long standing who had unfortunately fallen into bad company”. This in turn led to James Gillray’s famous cartoon entitled Political Ravishment; or the Old Lady of Threadneedle Street in Danger, which depicts Pitt seducing the Bank of England, personified as an old lady attired in £1 and £2 notes, for her fortune.[7] This cartoon is the origin of the Bank’s nickname of “The Old Lady of Threadneedle Street“, still in use today.”

William Pitt the Younger, in my opinion Britain’s second most destructive Prime Minister, would introduce the world’s first income tax in 1798, and would also sever England’s link to gold collateralisation of the private banking network for a generation, Pound Sterling would lose 90% of its purchasing power, and Britain would be hostage to Nathan Mayer Rothschild by the end of the Napoleonic Wars (1803-1815)… The period of Restriction would also “co-incide” with the beginnings of Britain’s meteoric population boom and the second half of the industrial revolution that would introduce steam locomotion and railways to the rest of the world…

After rising on average one million people per century between 1100 and 1800, England’s population explodes from 8.3 million people at the 1801 Census, to 30 million people by the 1901 Census (source)… It is no co-incidence that within a year of the Bank Restriction Act 1797, Thomas Malthus would publish his Essay On The Principle of Population in 1798, and his principle of the Malthusian Trap…

Thus was spawned Britain’s great empire building machine, founded on the removal of gold as collateral for a period of 24 years that would unleash upon Britain an energy revolution, agricultural revolution, industrial revolution and child labour revolution… The biggest capital misallocation of all in de-pegging purchasing power from scarcity and a sound anchor, and the underlying reason for Britain’s population explosion was not progress, wealth and the organic breaking of the Malthusian Trap as touted by Classical Liberals, Utilitarians and Whig Theorists of Historical Progress, but regress and poverty… The population explosion was the requirement for a rapid increase in fertility and larger families for the underclasses, exclusively for work and labour (to work the machines), to counteract the inflation and staggering loss of purchasing power of the currency and the crushing taxes to fund Britain’s domestic industrial machine, for its foreign Wars and World Empire…

1850 – Peak British Empire and Dismantling of the Corn Laws

Tariffs: The Taxes That Made America Great – Pat Buchanan

It can rightfully be claimed that the greatness of Britain and its Empire was built upon Mercantilism, that is tariffs, customs barriers and trade surpluses that the British government could recycle into the Royal Navy, that would protect by force and fire all of the above… Ironically it would be British mercantilism and customs barriers in the American Colonies, forbidding free trade with the rest of the European Continent, that would be one of the major instigators of the American Revolutionary War (1775-1783) and the British loss of its colonial crown jewel… Even so, the first half of the Nineteenth Century would see Britain’s Mercantilism and power peak, and with the dismantling of the Corn Laws in 1846 would convert to Adam Smithian and Liberal free trade ideals, which expanded the growth of Sterling as the World Reserve Currency of the Nineteenth Century, while running the trade deficits that built up its main two international competitors, the US and Germany… With the consolidation of the “United” States following the Civil War (1861-1865) and Bismarck’s founding of the German Empire in 1871, Britain would undermine its own productive economy and competitiveness by building up the productive economies and competitiveness via trade surpluses, of the Mercantilist US and Germany into the 20th Century… Germany and the US would also import the British Central Banking model during this period, with the Reichsbank founded in 1876, and The US hoodwinked into the Federal Reserve Act of 1913, just in time for the ultimate expression of the industrialisation spawned during the Nineteenth Century, the industrial wars of the Twentieth Century…

World War I – Something’s Gotta Give

Britain’s disastrous policy of running trade deficits with its two major exporting competitors would diminish British Power to such an extent, by the turn of the 20th Century (eerily reminiscent of today’s relationship between the US and China), the War Drums inside Britain rose as Germany threatened its European dominance with its own 30 year and budding Empire, you can think of World War One as Britain’s successful decapitation of a rival, while also sabotaging its own future as world power… The War on Germany geopolitically and diplomatically had been waged by Britain since the birth of Bismarck’s Empire, but one of the most undertalked events of the first decade of the Twentieth Century was the Triple Entente, and divide in the historic alliance between Germany (Prussia) and Russia, which would just over a decade later bring to an end both their monarchies, and on the brink of Communist (Democratic) Revolution… While the emergent German powerhouse would have been confident in the defeat of France and Russia and enlarging their Empire some more in a traditional Continental War, they had not reckoned on the kamikase actions of First Lord of the Admiralty Winston Churchill and Britain’s most disastrous statesman, entangling Britain in a World War that would decimate the British and German Empires, leaving the US as the only realistic World Power following 1918…

Time to foreclose on the Churchill Cult

1920’s – Salvaging The Gold Standard

The co-ordinated abandonment of the late 19th Century Classical Gold Exchange Standard by the West’s Central Banks (outside of the US) in printing the First World War, would unleash inflation, shortages and rationing over all of Europe, and so the 1920’s was the decade of trying to return to the Standard of Gold, to varying degrees of success… Germany’s War debts (denominated in gold) had created the hyperinflation of the Weimar Republic in the early 20’s as they did not have gold to back the Papiermark, and during Winston Churchill’s stint as Chancellor of the Exchequer, Britain’s Gold Standard Act 1925 would remove gold coins from public circulation, for a Bank of England banknote standard backed by Gold Bullion… Alas, dear old Winston would fix the gold price at the Pre War rate of $4.53 per pound sterling, creating a deep depression and the General Strike of 1926, and the British would be forced back off gold soon enough…

1930’s – Gold Demonetisation and Confiscation

As the Roaring Twenties and its credit fueled debauchery of American and European economies came to a catastrophic end with the stock market crash and banking collapses throughout the West, the 1930’s would bring with it the rise of authoritarianism and the decade which gold and silver coins would be phased out and confiscated, further subordinating Western economies to credit and debt…

A bank run on Austria’s largest commercial bank, Credit Anstalt in May 1931 would cause its collapse, forcing Germany and Austria to suspend gold convertability, then enforcing exchange controls by the Autumn, which would lead to a run on Sterling, and from September would force the Bank of England unilaterally and abruptly off the gold standard “temporarily”… Australia and New Zealand had already left the standard and Canada quickly followed suit, and by the end of 1932, the gold standard had been abandoned as a global monetary system… Czechoslovakia, Belgium, France, the Netherlands and Switzerland abandoned the gold standard in the mid-1930s…

With the carnage of the beginnings of the Great Depression (really credit unwind), that threatened the solvency of a large swathe of US banks, on the 9th of March 1933 Congress approved the Emergency Banking Act, aka the Glass-Steagal Act, centralising America’s banking industry and giving the 20 year old Federal Reserve System a lot more power… The Banking Act would also sever convertibility between treasury notes and gold, setting up the most audacious gold heist in world history in the following months…

Following the sucker punch of the Emergency Banking Act, the knockout punch came on 5th of April 1933, with Franklin Delano Roosevelt’s Executive Order 6102, and the Great gold confiscation of the Continental US… Americans would be compelled to turn over their gold coins, bars and certificates over to the authorities at $20.67 per ounce, prior to the revaluation of gold to $35.00 per ounce, or otherwise stated a a near 50% devaluation in the purchasing power of the US Dollar against everybody who had turned their gold in… Great Depression indeed!

WWII – US Hegemony Consolidated

Portuguese Propaganda Poster depicting the European fight against Communism, and its Anglo enablers…

The Second World War was in many ways the final conclusion of the carnage created in the First World War… The Communist threat that haunted the European Continent from Russia’s Bolsheviks in the East had led to the establishment of European Nationalism and anti-communism, first in Italy under Mussolini’s Fascism, the hyperinflation of the Democratic Weimar Republic of Germany had led to the rise of Hitler and National Socialism, and Spain’s Red Scare had led to the rise of Franco following the Spanish Civil War… Hitler’s rebuilding of the German economy would unleash industrialism and militarisation for the invasion of Poland and France to regain the territories and populations lost to the Allies in the First World War, while anticipating the future push that would come out of Stalin’s Soviet Union in their attempts to spread Communism to the whole of the European Continent… Both the Nazis and the Commies would invade and divide Poland and set up the Eastern Front in what was another Continental War, prior to the entrance of the British and the Americans on the Western Front to divide Hitler’s forces, and ensure that Stalin and the Reds would enslave the population and territory of Eastern Europe up to the (future) Berlin Wall…

1944 – The Bretton Woods Gold Exchange Standard

In 1944 with the War already largely won, the Allied Powers convened at the Bretton Woods Conference for a global currency reset, and it would be decided that the role of global policeman and world reserve currency status would transfer from the bankrupt British Empire and the Bank of England, to the US Empire and The Federal Reserve System… British and European self sabotage and war economies had created massive trade deficits with the US, and by 1945 the US was the only remaining World Superpower, and held 75% of the world’s gold reserves, it really was a no-brainer that the US would take control of the world… The US Dollar (read Federal Reserve Note) would be (miraculously) pegged to gold at the 1933 ratio of $35.00 per ounce, and would allow British Pounds, French Francs, and German Marks (not backed by anything) to be exchanged for this gold… The Bretton Woods Standard that could only be described as the most bastardised and unsustainable of gold standards, at least provided some stability for the European Countries that had destroyed themselves through war…

Economic Fallout of World War II

Winston Churchill’s Greatest Quotes – purely for comedic purposes…

Further ignominy would befall the British outside of the loss of world reserve currency status, in the loss of Empire… While the British Empire had peaked in territory and population following the First World War (and it’s influence in the Middle East and Africa following the destruction of the Ottoman Empire), by 1945 Britain had squandered its military and gold and could no longer keep a control of its colonies… India would gain independence (and the partition creating Pakistan) in 1947, Burma and Sri Lanka would gain independence in 1948, the British would also exit Palestine in 1948… The Suez Crisis of 1956 would fully expose Britain’s loss of power in the Middle East and Africa, would lose Egypt in 1952, Sudan in 1956, Kuwait in 1961, and Bahrain, Qatar and the United Arab Emirates in 1971… Most of Britain’s Caribbean colonies were granted independence by the mid 1960’s, and its remaining African Colonies by 1968…

The Controlled Demolition of the Empire on which the sun would never set – the twenty five years between 1945 and 1970

1971 The Nixon Shock – The End Of The Gold Standard

The US spent the Fifties and Sixties hemorrhaging the gold reserves built up from the rest of the world during the first half of the Twentieth Century, as trade surpluses had morphed into trade deficits (and Triffin’s Dilemma) and the Vietnam War and Guns and Butter spending had led to an “Allied” run on U.S. gold reserves… Instead of explicitly defaulting on the horrendously thought out and constructed Bretton Woods Gold Standard, the US just defaulted implicitly on the gold part, so Nixon closed the gold window and the US Dollar (read Federal Reserve Note) would become unchained from gold, as would the rest of the West’s and the world’s currencies on what would now be a floating global exchange standard…

That was the Nation State/Central Bank explanation of the last few centuries, I will further pick up on the Great Inflation since 1971 in the next discussion of the private Banking System and Network, that precedes and exists outside of although not free from the influence of, Nation States and Central Banking…

A Brief History of Banking

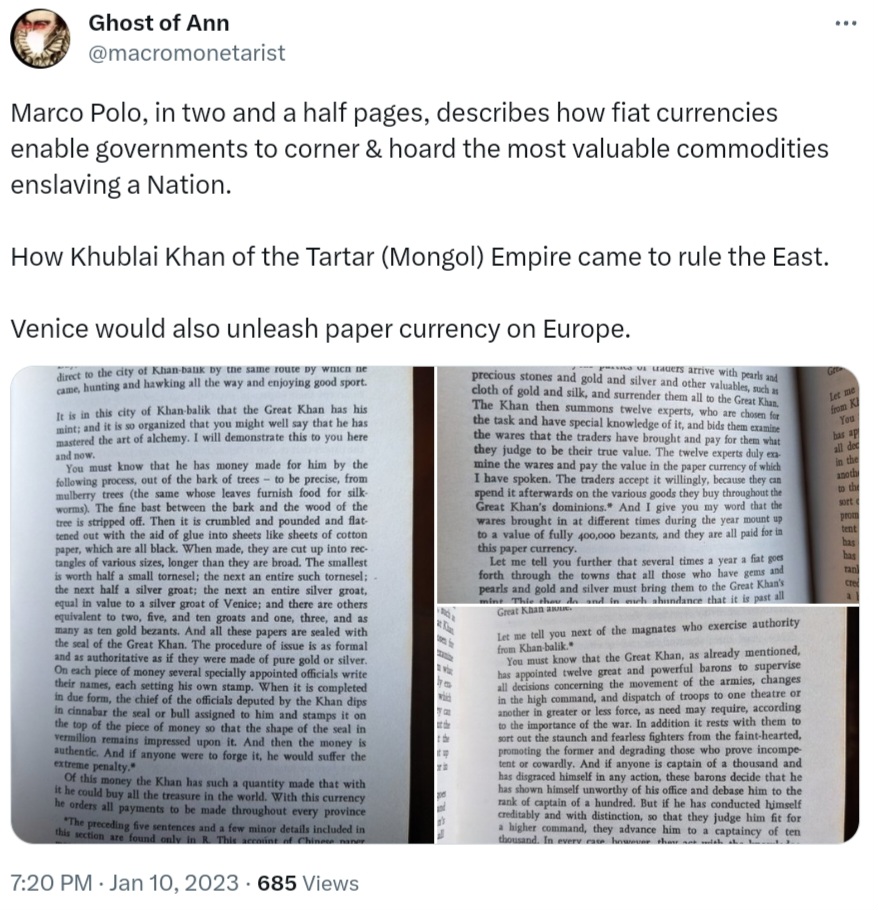

It was the Venetians (through Marco Polo) that imported paper money and cash from the East, and from previous posts I have also detailed the development by Northern Italian City states of the Double-Entry Book-Keeping Ledger at the end of the European Middle Ages… This double whammy of technological development, that of an accounting ledger that could track incomings (deposits, debits) and outgoings (loans, credits) and the addition of paper money or promissory credit notes as a far more convenient and scalable medium of exchange for European merchants, would underpin the Renaissance that spread throughout Northern Italy during the Fifteenth Century, and the European Reformation of the Sixteenth and Seventeenth Centuries…

Bullion Banking/Fractional Reserve Banking

While Bullion Banking and Fractional Reserve Banking would be pioneered by the Amsterdam Wisselbank in financing the Dutch West Indies and East Indies corporate monopolies that was the effective Dutch Empire, by the 19th Century London had overtaken Amsterdam as Europe’s financial centre, especially by the end of the Napoleonic Wars (1803-1815)… Gold would therefore be crowded out over time by waves of Credit that created the destructive boom and bust business cycles of the 19th Century, as observed by the British Currency School and was the foundation of Marx’ Communist Manifesto (1848) and critique of capitalism, and would increasingly be fractionalised by an unhinged banking system and reduced to mere collateral in inter-bank accounting…

1844 would see the Peel Banking Act, and the effective nationalisation of British banknote issuance by the Bank of England and tied to gold reserves at the bank, reining in private banknote issuance in a so-called victory for the British Currency School, who had long argued that private banknote issuance drove inflation… While this Banking Act consolidated Pound Sterling as the national denominator for British private banks in currency, the Act did not stop private banks creating deposits and loans, otherwise stated creating further credit based upon fractional reserve collateral… So while British banknote issuance was constrained, this did not prevent the banks working around this impediment by creating further fictional ledger credit and debt…

The second half of the 19th Century would see the development of international finance and financing, with London and especially the Rothschild family, alongside the Bank of England funding infrastructure for the British Empire (for example the 1875 purchase of 44% of the Suez Canal), and London serving as a financial hub for the rest of Europe in financing its industrialisation, especially railway networks…

20th Century

The Twentieth Century would see the increasing abstraction of Credit and currency initially among the rich elites, but would seep down to the middle and working classes as the Century progressed… While national trade surpluses and deficits would still be settled in gold bullion (at least until 1914 and the first World war), within domestic banking systems of the major world powers (UK, US, Germany, France), inventions such as cheques and other promissory and purely abstract ledger entries had largely replaced hand to hand money (i.e gold and silver coins)…

Cheques

While cheques qualify as a Bill of Exchange and therefore originated in the late middle ages alongside public banknotes, they were also popularised during the late 19th Century as a private substitute between banks, and especially among the rich… Cheques therefore could allow large value transactions to clear among banks and credit unions by the simple use of a paper ticket, without the transfer of any physical coinage which aided in the debasement of purchasing power and further disintermediation of hand to hand money during the early Twentieth Century, although mostly domestically within banking systems… Cheques would largely not solve the problems of transferring inter-bank ledger money internationally, which necessitated the invention of an international cheque system, which leads us to the Banker’s Acceptance…

International Banking – Banker’s Acceptance

The Banker’s Acceptance was one of several instruments used to finance international trade, and created in 1913 by the Federal Reserve to help U.S. banks compete with London banks in the international financing arena… Banker’s Acceptance offered several benefits, including being short-term instruments between trading countries (180 days or less), each was tied to a specific self-liquidating transaction, and could be sold on the secondary market (and still maintain liquidity)… The Federal Reserve specified certain transactions that qualified for BA financing, such as shipments of goods or secured with readily marketable commodities stored in independent warehouses…

The EuroDollar

There are a few Origin Myths regarding the Eurodollar, including the first Eurodollar account being created in France in 1949 as a method for Communist China to hold US Dollar reserves outside the reach of US government confiscation, also an English bank establishing an Eurodollar account on behalf of the Soviet Union in 1956 after the invasion of Hungary… In either case, the origin of the EuroDollar was the creation of Dollar accounts and deposits outside the United States, and therefore outside the regulatory reach of the US government in case of confiscation by hostile powers…

These markets for Eurodollars would flourish throughout the Sixties as the Bretton Woods Gold Exchange Standard neared its end, and predominantly situated in Europe and its financial trading centres, the City of London, Zurich, Switzerland, and Frankfurt, Germany… By the end of 1970, 385 billion Eurodollars were held in offshore bank accounts, and these deposits would be lent on as U.S. dollar loans to businesses in other countries where interest rates on loans were perhaps much higher in the local currency, and where the businesses were exporting to the U.S. and receiving payment in dollars, thereby avoiding foreign exchange risk on their funding arrangements…

By the 1980’s Eurodollars had overtaken certificates of deposit (CDs) issued by U.S. banks as the primary private short-term money market instruments for several reasons, including the successive balance of payments deficits of the United States causing net outflows of dollars, Regulation Q, the Federal Reserve’s ceiling on interest payable on domestic deposits during the high inflation of the 1970’s, and Eurodollar deposits were a cheaper source of funds because they were free of reserve requirements and deposit insurance assessments…

Since the Eurodollar market is not run by any government agency its growth is hard to estimate, however the Eurodollar market has become by a wide margin the largest source of global finance, and by 1997, nearly 90% of all international loans were made this way…

In December 1985 the Eurodollar market was estimated by J.P. Morgan Guaranty bank to have a net size of 1.668 trillion and in 2016, the Eurodollar market size was estimated at around 13.833 trillion…

The Eurodollar has also spawned a sprawling market of offshore derivatives, in Eurodollar Futures launched on the CME (Chicago Mecantile Exchange) in 1981, and tied to three months LIBOR rate…

The Eurodollar is probably the biggest banking corruption development in the history of finance, and so I feel the need to go into this in further depth, as it has undemined Central Bank and Nation State authority and power since the end of the Second World War, it created the post 1971 globalisation of the world and monumental shifts in capital and even populations, and huge imbalances in trade shifts from deficit running Western Countries, to surplus running Eastern Countries… Indeed it could be argued that the current Western push for CBDC’S is an attempt by Central Banks and National Governments to take back national control of what is truly an international financial system, nationalism also plays into another recent geopolitical theme of re-shoring of Western Corporations and supply chains, as National Security concerns are feeding de-globalisation, and further fracturing of the Seventy year old Eurodollar…

The Rise Of The Eurodollar (1970-2007)

While the Eurodollar and Dollar based offshore or shadow banking was born in the Fifties, it was in the Sixties that its growth would threaten the Bretton Woods gold exchange standard, and despite all the shenanigans of the Anglo-American and Europeans via the London Gold Pool to manage the price of gold and stem the bleeding of US gold reserves, the US through Nixon had to close the Gold Window and its obligation to pay the rest of the world’s Central Banks in gold, but in Dollars… However the flipside of this coin was that the growth of the Eurodollar System that broke the Bretton Woods Agreement was because of European Central Banks creating Dollar liquidity outside the US while also circumventing the limits of gold, and so by the time Nixon closed the Gold Window this Eurobank networks of Central Banks and Commercial Banks already had a long running alternative that they had seamlessly adapted to, and gold as even fractional collateral could be quietly removed from the monetary system…

From here on I will defer to Jeff Snider, Eurodollar Historian and Economist, and his excellent 2013 three part primer on Understanding Eurodollars (Part one, two and three)…

The Eurodollar explosion during the Seventies would intermediate importers and exporters of a rapidly globalising world, and would lead to debt crises in some developing countries on the peripheries…

While the Seventies had seen an explosion of Eurodollars offshore and outside the US, the Eighties would see Eurodollar explosion onshore and inside the US – aka Financialisation…

The Nineties sees the integration of Eurodollar financial centres, especially between New York and London, and the expansion of balance sheets of all large global banks…

Huge Eurodollar credit expansion during the 2000’s would blow up all sort of asset bubbles, which preceded the monetary breakdown of 2007, and the financial crisis of 2008…

The Digitisation of Banking/Finance

While the development of Banking history happened initially through precious metals and later through paper substitutes, the digital revolution that has enveloped the world in the second half of the Twentieth Century has obviously had a massive effect upon the Banking and Finance industry, wherein the entire Eurodollar and derivatives complex that is now undeniably (but still unofficially perhaps), the de facto world reserve currency, is near exclusively by now computerised and digital, finance today runs on digital ledger entries on bank computer screens that rules the world and is completely abstracted from any underlying physicality… These development of messaging networks such as SWIFT (that still accounts for half of High value transactions in the world as of 2018) started as Telex (manual writing and reading of messages), by now has completely embraced the Internet and allows banks worldwide to adjust their own ledgers and balance sheets through computers and the world wide web…

The Fall of The Eurodollar (2007 onwards)

The Eurodollar crisis began in 2007 with a breakdown in trust between the private banks, which eventually forced the Central Banks to intervene in 2008 with Quantitative Easing…

For the traditional and mainstream view of Quatitative Easing as “Money Printing”, the reality is that QE is an asset swap, Central Banks create bank reserves in exchange for collateral such as US Treasuries… And as US Treasuries have benefits over Fed bank reserves as more fungible inter-bank and financial collateral, perversely QE took UST’s out of circulation, making collateral shortages worse, creating the dollar and liquidity shortages that have plagued the global Eurodollar ever since!

US bank usage of Eurodollars collapsed at the Start of QE2 in November 2010, while foreign bank usage also dropped…

The more Fed QE’s, the more the Eurodollar withers… The evidence is compelling…

Eurodollar post 2008

The US credit creation machine broke in the middle of 2007 and has gone nowhere since, reflected in stagnating US economic growth ever since…

The breakdown of the global Eurodollar System, aka the World’s Silent Depression since 2008, can be best expressed via National Economies, who have all suffered since be they in the West or the East… Eurodollar shortages is just a fancy way of saying that the private banking credit machine that creates all the loans and credit to fuel “economic growth” has been spluttering and malfunctioning since 2008, which shows up in National Economies as lower GDP growth and numbers which has fuelled economic weakness, national public discontent, leading to the fracturing of the global economic system, mainfested as rising nationalist and anti globalist sentiments, as we have seen with the Brexit and Donald Trump double whammy in 2016, and China’s shift at the 19th Party Congress of the CCP in 2017 towards qualitative over quantitative growth, and the reduction in credit creation that has also been called “managing decline”…

All the following charts sourced from this article: Eurodollar System: The Untamable Beast…

The shifting baseline of GDP growth since 2008 (thick red line) may not look huge, but it has had an enormous effect on the American economy, American workers, and American families… I would argue this stagnation during the Obama Presidency 2008-2016, led to the Election of Donald Trump in 2016, based upon Making America Great Again…

Europe’s baseline GDP falloff (thick purple line), has suffered even worse than the US, reflected in the increasing fracturing of the European banking system and the EU, that accelerated with Brexit in 2016…

China has suffered the same from Eurodollar shortages, as the PBOC uses incoming dollars on the asset side of the balance sheet, to fund its yuan liabilities on the credit side, and the Dollar/Yuan managed peg… Dollar shortages equals Yuan shortages, exarcebated by the near three year long Covid lockdowns in China, leading to deteriorating economy, falling house prices and increasing youth unemployment… The Eurodollar crisis is also ultimately behind the recent moves by the BRICS to attempt to decouple from the Eurodollar, and rumours of a new gold backed currency system... We shall see…

Squaring The Circle – Reconciling Central Banking with Private Banking

After the above detailed explanation from the Nation State centric angle and from Eurodollar global centric angle, how do we reconcile these conflicting narratives and explanations for the last century of monetary history? After all, if you submit to the Eurodollar version of history, then Central Banks don’t print money and neither are they central to the financial system, rather national currency denominations are merely symbolic for a banking system that has long been working outside national borders and has been global for at least the last fifty years… Eurodollar proponents will tell you that Central Banks work exclusively by psychology, merely printing inert bank reserves for the private Banking system that is the real credit creator out there in the real world wide economy…

So if Central Banks are not central, and do not print any money that ends up in the real economy, then what is the actual relationship if any, between Central Banks and the Eurodollar, today?

Collateral

So we arrive at, in my opinion at least, at the truth within the monetary system and where the rubber meets the road between Central Banks and the Eurodollar, and between National Banking and International Banking, which is collateral…

While I would agree with Eurodollar proponents that the global monetary is system is undeniably the Eurodollar, that is a decentralised, reserveless, worldwide inter-bank dark web of ledger entries on bank computer screens and balance sheets that works independently from the world’s Central Banks, the Eurodollar has evolved in the Golden Age of Central Banking and The Nation State, and so is still dependent and constrained by National and International Laws and Licences in the Banking and financial industry, and regulations and regulators of these Laws… So while Central Banks are completely at the margins in terms of real economy credit creation, the Eurodollar is still reliant on Central Bank collateral in Bank Reserves, and National Governments in the bonds they issue…

The evolution of the Eurodollar therefore was the replacement of gold as primary collateral for the worldwide banking system, and its replacement by the bonds of National Governments… This has been achieved largely by force, as even individual private banks operating within the Eurodollar global system are still tied to Nation State governments and Central Banks, who by power of Law can mandate that banks invest in their debt as the most liquid and pristine collateral underpinning their book-keeping ledgers and balance sheets…

These Are The Largest Bond Markets In The World (Source)

Central Banks therefore act as intermediaries between Government Treasuries and Eurodollar financial institutions, distributing collateral through the financial system as liquidity for extending loans and expanding balance sheets, and economic growrth…

Collateral Shortages Post 2007

Swiss Eurodollar Conduit: UBS as proxy for Eurodollar breakdown

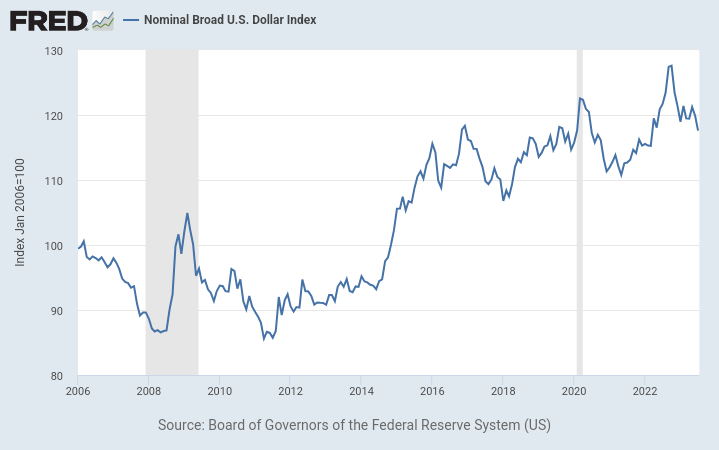

As already discussed, the Eurodollar reached its peak in 2007, a year before the Great Financial Crisis of 2008 and from which the Eurodollar never recovered, especially in Europe and European banks, with former Eurodollar conduits such as the just defunct Credit Suisse and UBS of Switzerland, Deutsche Bank of Germany, French, Italian and British Banks have all suffered and shrank in size since 2008, as Eurodollar collateral and liquidity dried up and has never really returned… Since 2007 there has been persistent collateral shortages that have co-incided with “Strong Dollar” episodes when the US Dollar Index strengthens against other fiat currencies, indicating a scarcity of Dollars…

The US Dollar Index was 90 in 2008, it it around 120 today… https://fred.stlouisfed.org/series/DTWEXBGS#

The Debasement of Collateral

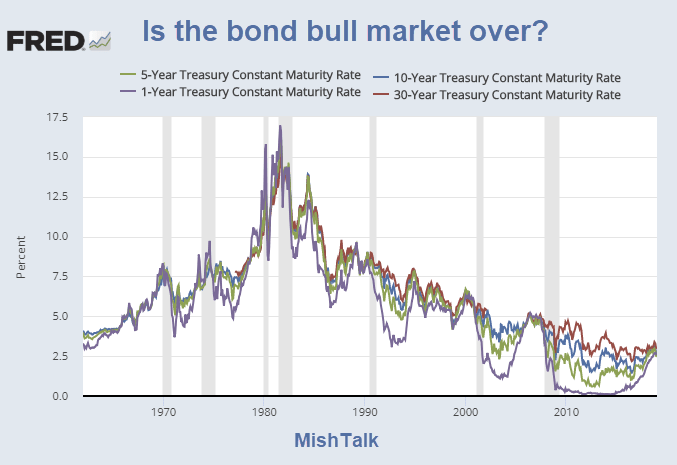

While the collateral underlying the Eurodollar System is incredibly varied and complex, it is mostly underpinned by Government Bonds, especially US Treasuries but also British Gilts, German Bunds, French, Italian and Japanese Government Debt (see above bond maket chart)… It is also undeniable to me that the quality and utility of the global collateral pool has been declining since the Seventies, also expressed in the surging issuance of government bonds and debt, and the declining yields making bonds a worthwhile proposition… Governments have never been more bankrupt today, and yet their legislative power over forcing Eurodollar banks through balance sheet regulation to hoard their bonds and debt, and aligned with increasing Central Bank meddling in mostly suppressing short term interest rates has led to the great bond bull market of the last forty years, but which has made the global financial system ever more unprofitable, and never more unprofitable than it has been since 2009 and the ZIRP/NIRP and QE era… And while Western Central Banks have in the last fifteen months been hiking rates at the short end to eyebleed levels for a world so saturated with unprofitable and debt laden companies and corporations, they have already triggered the next banking crisis that will contract trust, inter-bank lending, and credit creation to the Western and by extension global economy, I predict that in 2024 and 2025 Central Bank interest rate setting will return to zero and negative, as a result of the recession/Depression their actions are creating…

Is the Forty Year bond bull market over, and are we going back to the Seventies? Personally, I doubt it...

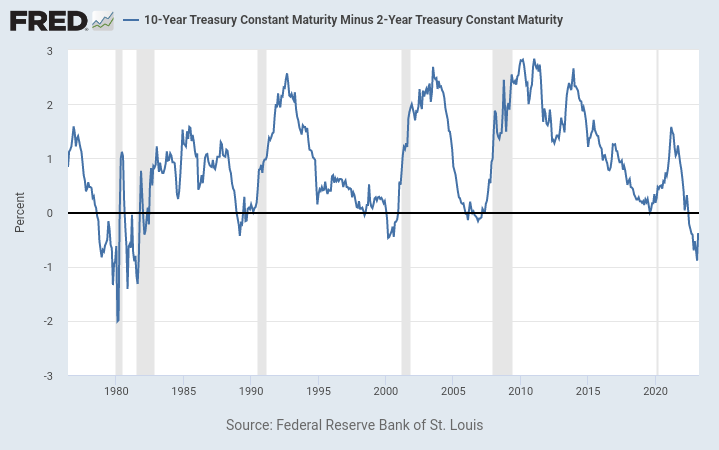

In addition to the “reach for yield” that ZIRP/QE has engendered since the Financial Crisis, I have also talked in past posts about Yield Curves, and especially the US Treasury Yield Curve as the ultimate expression of global “risk-free” collateral, and the proxy for Net Interest Margins that is still a critical component of modern banking, the margin between short term borrowing and long term lending, otherwise stated the profitability of money for the global Eurodollar banking system…

Note how yield curve inversions precede recessions (grey areas)… The 2s 10s yield curve has been inverted since April Fool’s day 2022…

As the above chart demonstrates the margin between 2 year and 10 year US Treasuries has been under 2% since 2015, and while it did not quite invert in 2019 before the Covid Crisis, it has been deeply inverted the last year, and is only now starting the steepening that will usher in this or next year’s global economic recession, and the real hangover of the Covid craziness of the last three years… It should also be obvious that an inverted yield where shorter term and less risky debt is yielding (risk premium) more than longer term and more risky debt, craters Net Interest Margins and Net Interest Income, and the profitability of Banking… So not only is the quality of collateral diminishing in yield, but the yield curve is further strangling the profitability of the whole global financial system sitting on top of it…

The final degradation of collateral we need to discuss is the quantity of the collateral underpinning the Eurodollar, and which has never really recovered since the financial crisis, indeed the persistent collateral shortages post 2008 are critical in understanding why the whole financial system hasn’t bounced back for the last fifteen years… There are many ways to approach this quantitative aspect, initially starting from the de-risking of bank balance sheets after 2008, away from unsecured lending toward secured lending, governmental and banking regulation that has contributed to the crowding out of more risky (and abundant) forms of private collateral toward less risky (and scarce) forms of public collateral, i.e US Treasuries… The Federal Reserve policy of QE may have also exacerbated this shortage of collateral by issuing bank reserves in exchange for buying US Treasuries, and effectively removing more fungible and liquid collateral (UST’s) and adding less fungible and liquid collateral (FED bank reserves) onto which the Eurodollar’s credit creation system is dependent! For a combination of complex reasons the shrinking of eligible collateral created by Central Banks and Governments has shrunk the combined balance sheet of the Eurodollar shadow banking network, which translates into the real economy as weak economic and GDP growth worldwide, creating chronic Dollar shortages outside the US which is creating carnage in Europe, China, Japan, Latin America and Africa…

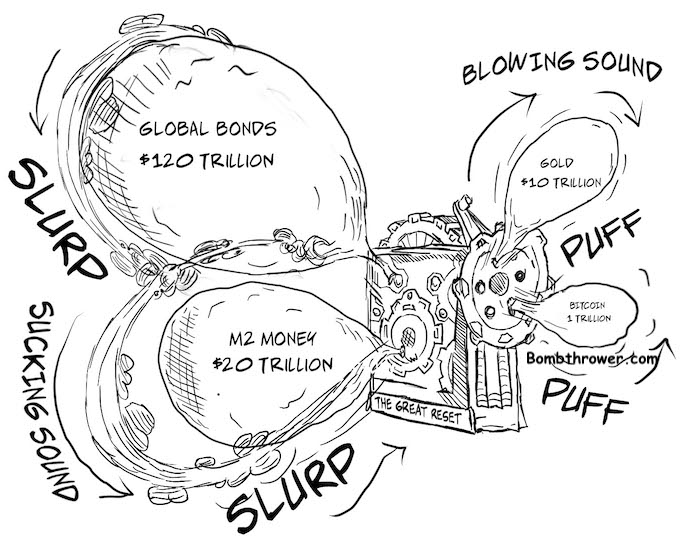

In conclusion, today’s global financial system is stuttering and spluttering because of chronic shortages of collateral to pledge in expanding Eurodollar credit creation worldwide, thus growth post 2008 has not recovered and is fueling the continuing economic unrest worldwide, and this collateral is principally issued by National Governments that has been degrading in quality, in margin, and quantity… In short, lower yields, lower net interest margins and a shrinking pool of usable collateral is slowly destroying the financial system, and this I argue is because of Central Bank manipulation of short term interest rates (ZIRP) that has inhibited profitability, risk taking, entrepreneurship, and capital formation at the short end, which is inhibiting capital formation and risk taking at the long end… While this deficit could perhaps be cured by the interest rate hikes that Central Banks have engaged in the last 15 months at the short end if it lasted for the next few years to start feeding into the long end, as we are seeing now the financial system is so addicted to cheap money and low interest and debt service costs, that the financial system is in the process of blowing up and so to save the day again, Central Banks will have to eventually go even deeper into ZIRP/NIRP and QE, which will further exacerbate the collateral shortages and the further contraction of the Eurodollar and all the societal destruction worldwide… As I have made clear in all my posts the whole financial system worldwide is in terminal decline under the current order, and so the re-capitalisation and re-birth of the global financial system will have to come from outside the debt based system, and from the non debt based world…

The New Collateral – Gold and Bitcoin

And so, after a long but very necessary discussion of all the above, we finally come to the new collateral, that is both old and new, and both Proof of Work systems in a world of Proof of Stake… The achilles’ heel and ultimate destroyer of Proof of Stake is centralisation, as over time the tendency is for the Stake to concentrate in less hands until a monopoly develops, and the exploitation of the many by the few, while Proof of Work is a far more distributed method of production that can maintain decentralisation of money and power far greater than what has happened since the Age of Banking… The fact that neither gold nor bitcoins can be created from thin air gives them a scarcity that will appreciate over time, at the polar opposite of devaluing government bonds valued in fiat currencies…

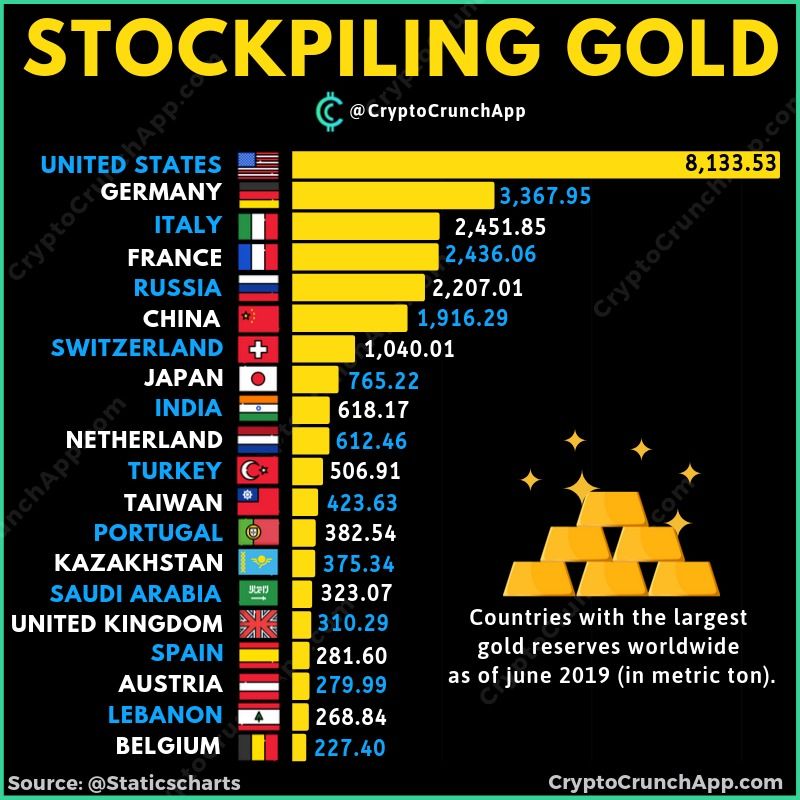

Old Collateral – Gold

Whether you believe Central Bank and Governmental accounting of gold reserves or not, I’m just working from the figures being reported by them, up to June 2019…

In a world of collapsing long term bond and collateral values, an easy call to make is that world governments will re-value gold upwards while also expanding its scope as collateral for the Eurodollar system… This is as simple as accounting rule changes on financial and bank balance sheets, and the great advantage of gold is that it is already the historical foundation of the five century old double-entry book-keeping and fractional reserve banking model, and is relatively evenly distributed between the world’s central banks and national governments, as the above chart demonstrates… As the last five centuries, and especially the last two centuries has been the de-monetisation and fractional collateralisation of gold, the future I believe is the re-collateralisation of gold as balance sheet asset…

The last ten years has seen the world, especially China and Russia, stockpile less US Treasuries, and more gold (source)…

Since the Financial Crisis of 2008, Central Banks have been buying more gold in preparation for some kind of reset…

I have written a trilogy of gold and the blockchain posts, and in my post during the last months of the Trump Administration in 2019 speculated that the US Military was engineering a return to the Gold Standard, since sabotaged by the Covid Scamdemic and the Democrats blatant theft of the 2020 Elections, but maybe this was all by design anyway… The disastrous Biden Administration serving from January 2021 to November 2024 that has presided over the Covid Supply Shocks, the surge in energy and consumer price inflation that has forced the Fed into hiking rates that has created all the recent banking turmoil, and will unleash a historic credit crisis and recession/depression in the next couple years, will likely lay the foundations for Trump’s second stint from 2025 to 2029, and if the Republicans are able to dominate The House and the Senate, then he may be able to fulfill to a far further extent what he promised to do in 2016, and actually Drain The Swamp this time around… This will also take at least the next two years to play out…

Koos Jansen, whose work as a gold economist and historian I rate highly, has written for years on the likelyhood of Europe also returning to a Gold Standard, and I highly recommend his Two Part series on Europe Has Been Preparing a Global Gold Standard Since the 1970s (Part 1 and Part 2)… I add a few excerpts below…

In 1999, fourteen Central Banks agreed to the Central Bank Gold Agreement (CBGA), to balance gold reserves between European Countries, and also the rest of the world… Gold rich Euro countries mostly sold reserves to the rest of the world… The CBGA was extended three times, and ten more European countries joined… During CBGA 1-4 a little over 4,000 tonnes were sold, virtually all of which before 2009…

Western Europe sold their gold reserves mostly to Eastern European, Middle Eastern and Asian Countries, thus distributing gold reserves more equally between competing economic blocks…

Official gold reserves vs GDP…

From the above, there does seem to be collusion between Central Banks and National Governments in equalising gold reserves across countries and economic blocks in preparation for some kind of gold standard, however the extent and timing of the return to gold is unknown… Under a classical gold standard, trade surpluses and deficits would be fully settled in gold between countries, thus surplus running countries would accumulate gold from deficit running countries… This in turn should stimulate more consumption and imports in surplus running countries as gold is relatively abundant compared to goods and services, while the shortages of gold in deficit running countries should stimulate production and exports in order to get that gold back, and so the system should in theory be self correcting… However it should also be clear that as this gold cannot be created from thin air, it would severely limit fractional reserve banking and credit creation compared to the last seven decades of the Eurodollar system, and it would severely clamp down upon government debt issuance and deficits, collapsing the size of banks and governments down to a fraction of its current size… Indeed it was the limits of gold upon Central Banks and Governments, especially during times of War, that led to the abandonment of the Classical Gold Standard in 1914, morphing into the Interwar fractional Gold Standard of 1918-1944, and the Bretton Woods Gold Standard of 1944-1971… The return to the Gold Standard would also entail The US and UK largely giving up their trade deficits, financialisation and import orientated economies, and The Eurozone and the BRICS giving up their trade surplus, production and export oriented economies…

Gold Revaluation – Gold Fixing and The Gold Futures Standard

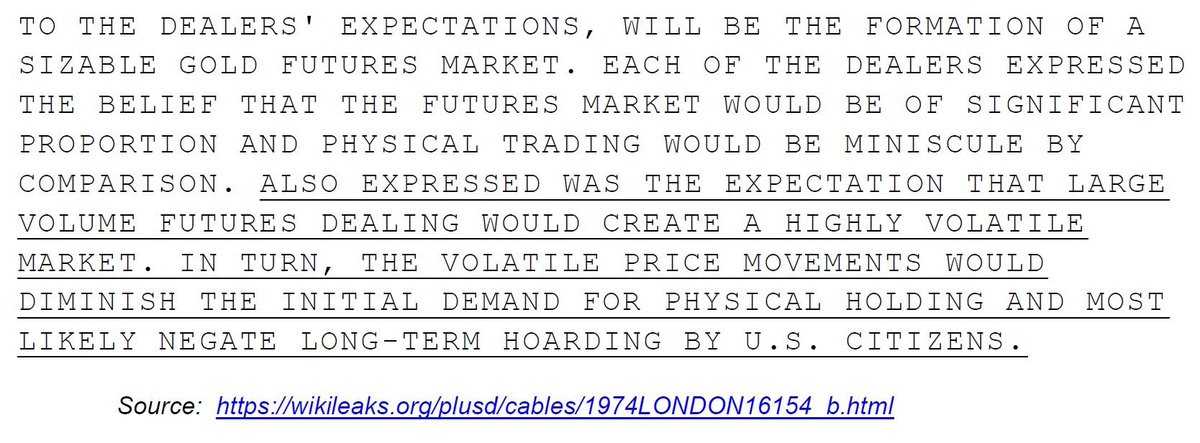

Wikileaks 1974 Cable Reveals Purpose of Creation of Gold Futures Market (H/T Smaulgld)

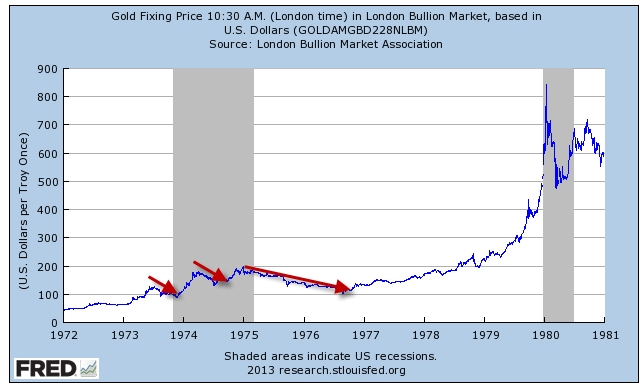

Even the serial abuse gold had suffered at the hands of the Banking industry during the first half of the Twentieth Century, was nothing compared to the ignominy suffered after Gold was legalised in the US, reversing the four decade Franklin Crime, on the 1st January 1975 Americans were once again allowed to hoard gold… While this did allow for use as a store of value, the medium of exchange function had been entirely subsumed by banking, in cash, cheques, and other paper derivatives, in short the financial system had moved further on… The Seventies and the great inflation of the Eurodollar fuelled the futures based gold price from $200 in 1975, initially dipped as futures worked their magic of price suppression, however between 1976 and 1980 would spike 6x to $850, and with waning faith in the purchasing power of the US Dollar, led to Reagan’s Gold Commission headed by Ron Paul, investigating a return to the Gold Standard…

As fast as gold had soared in the Seventies, it plummeted just as fast during the Eighties, and stagnated in the Nineties, hitting its generational bottom around the turn of the millennium… Gold would soar from the Dot Com bubble onwards, and breached $1,000 in the wake of the 2008 financial crisis, hitting a decade high peak of $1,800 in 2011, then falling from the Eurozone Crisis of 2011 as Central Bankers re-established some confidence for a battered fiat system, until the last few years when gold has established new all time highs at $2000, and looks set to go higher again from here, as the second great financial crisis seems to be on deck in the next few years…

Gold has exploded 10x in the last twenty years (Source)

The main global trading hubs of gold today are London, the historic centre of gold bullion for the last three centuries, through the London bullion market and trading between London Bullion Market Association (LBMA) members, that also sets the twice daily London Gold Fix, that sets the physical price… There is also gold futures trading on the Comex in New York, the Shanghai Futures Exchange and Shanghai Gold Exchange in China, which together with London have over 90% of global trading volumes, setting the price for producers and consumers worldwide…

Major Global Gold Trading Hubs as of 2021, according to the World Gold Council

Whether you believe that the futures tail wags the physical gold fix dog or not, as far I am concerned the historical rigging of gold through increasing fractionalisation is undeniable, indeed since The Origin of Banking has been the historical dilution and supersedence of accounting ledgers over monetary media, born at the end of the Middle Ages, progessing along with Protestantism throughout Europe first, and since spread to the rest of the world… The second great Protestant Empire was the British Empire, and as discussed earlier, from the Eighteenth Century gold was increasing fractionalised and diluted by banking ledgers and derivative paper currencies, since 1971 essentially the whole world has been living in a fiat bubble unmatched in human history, and an unprecedented era of rigging gold prices and much more importantly rigging gold narratives, among economists, academics, polititicians, bureaucrats and journalists that fabricate the reality of our modern world… However if you have also studied history, then you also understand that every government that went off a gold standard has eventually returned to a gold standard, as tempting as it is to believe “this time is different” and that the square has finally been circled, with Western Currencies and Governments increasingly failing I argue the West will be faced with the inevitable…

Basel III Accounting Rules – Gold promoted to Tier 1 Capital

Gold got another regulatory boost in the last two years, and from the Bank for International Settlements no less, when under the new Basle III Agreement, gold was revalued as a risk free Tier 1 asset, as long as gold is either held in their own vaults, or in allocated form… So this is a boost for holding physical gold reserves, and it disadvantages unallocated or paper claims on gold… The risk free status of physical gold should encourage central banks, banks and institutions to hold gold as balance sheet and book-keeping asset, and should further marginalise gold futures and unallocated gold instruments…

BRICS Gold Backed Currency

The latest hype with regards to gold backed currencies, is what the BRICS is allegedly planning and set to be unveiled between the Twenty Second and Twenty Fourth of August at the BRICS Summit, and a gold backed trade settlement currency to undermine and sideline the Dollar/Eurodollar in BRICS trade… This hype has hit fever pitch in the last year after the US seizing of $600 billion in Russian foreign reserves, has forced the BRICS and especially China (that would surely suffer the same fate should it invade Taiwan) to develop alternatives and workarounds for Western Finance, and as the BRICS are all major gold producers as well as major gold hoarders, it makes sense to me that gold will play a major part as alternative trade and banking backed collateral to US Treasuries and the perfidy of Western Governments… As China is also one of the three main global clearing markets for gold, via the SGE (Shanghai Gold Exchange) and the SHFE (Shanghai Futures Exchange), it is uniquely positioned to pressure London and New York in its gold pegging, which also ties in with the gold revaluation thesis…

My gold revaluation thesis is not predicting a return to the gold standard or the complete collapse of the Post WWII Dollar and Eurodollar, it is simply predicting that gold as the original foundation of the banking system will shine once more as over indebted governments faulter, that will force a revaluation of gold as underlying collateral, boosting the balance sheets of central banks and the banking/financial system in general, at the expense of the global bond and debt markets as collateral… The price of gold revaluation is government debt devaluation, reining in government spending and deficits, and puts soomewhat of a floor under the purchasing of national fiat currencies, and will drive physical gold ownership in the West (gold is already widely held privately in the East)…

New Collateral – Bitcoin

Bitcoin Genesis Block: The Times 3/Jan/2009 Chancellor on brink of second bailout for banks

While the history of gold and banking are eternally intertwined, Bitcoin has no connection at all to the banking system, existing rather as an internet native distributed ledger and currency system, launched as a one man project in the first days of 2009… Satoshi initially ran the miners and nurtured the network until his disappearance in late 2010, since then the project has progressed by a bottom up network of developers, miners, exchanges and users (hodlers) over the last fifteen years worldwide, that have scaled Bitcoin to where and what it is today…

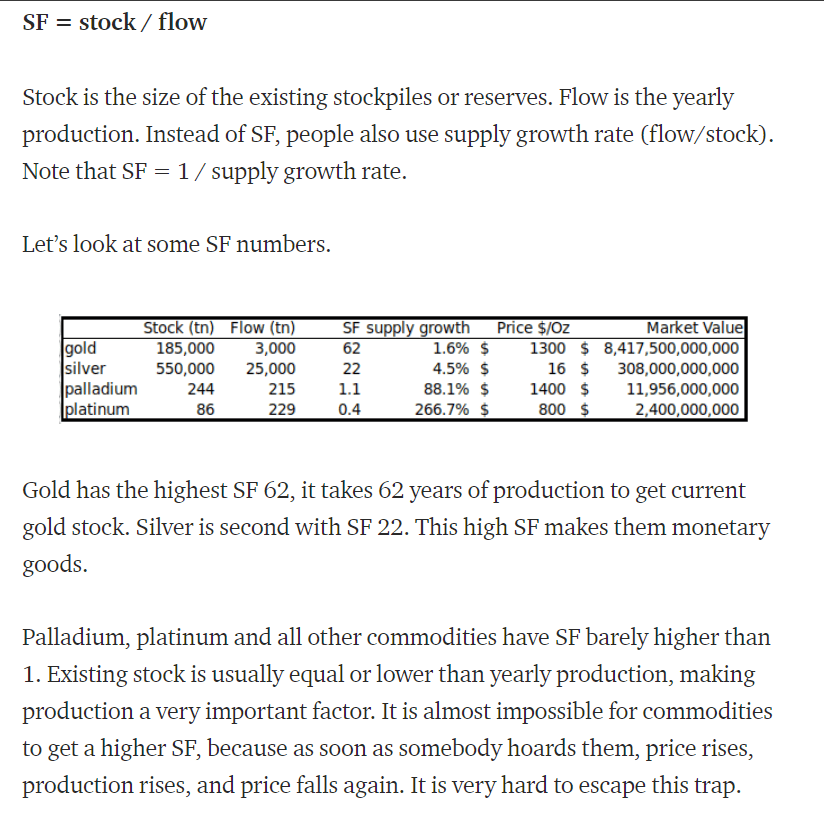

Bitcoin Versus Gold – Comparing Proof of Work

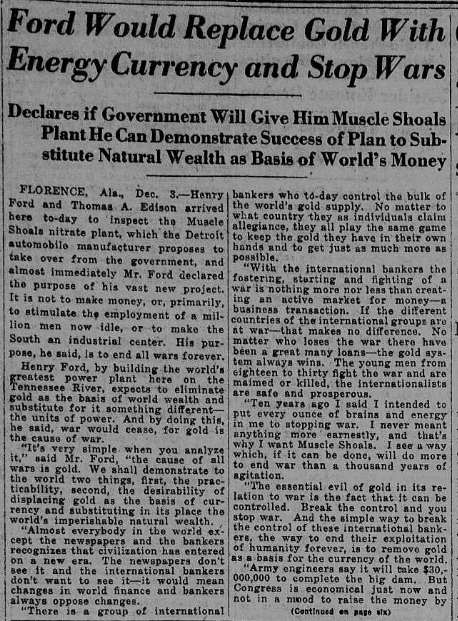

“Almost everybody in the world except the newspapers and the bankers recognizes that civilization has entered on a new era. The newspapers don’t see it and the international bankers don’t want to see it-it would mean changes in world finance and bankers always oppose changes.” – Henry Ford imagines an energy based Proof of Work system to replace the old Proof of Work Gold Standard that was hijacked by bankers and Proof of Stake during WWI… From the New York Tribune, Sunday, December 4th, 1921…