This post will conclude the trilogy of my Bitcoin Kills Banking posts and will again visit the discussion of the present in the dying throes of the fiat banking system that has ruled this last five centuries since the Reformation, and the rise of its nascent rival and eventual nemesis in Bitcoin, and will concentrate upon where they both connect which is exchanging and exchanges, and will discuss exchange prototypes and the regulatory developments that we are now witnessing as institutional (Wall Street) money starts to eye up the crypto sphere… Indeed throughout my Bitcoin Kills Banking series I have made it clear that our current banking system is in terminal decline, while Bitcoin I have argued throughout my posts since 2015 is a future world reserve currency and peer to peer payment processor that will obliterate the fiat banking system worldwide, therefore probably the most important discussion to be had in the world right now is about where both the legacy fiat currency systems and Bitcoin converge, at the exchange level…

Bitcoin Kills Banking – Summary

In my post published November 2015 I described the current post 2008 Weekend At Bernie’s financial system that had collapsed into default and insolvency, but had been kept visually animated by abolishing Mark to Market Accounting (FAS 157) so that busted banks did not have to mark their holdings to the market, they could maintain holdings in suspended animation thanks to Central Banks and their unlimited liquidity operations… By driving interest rates to zero and flooding the world with Quantitative Easing (money printing in short) the cost of capital and debt servicing costs was drastically lowered to allow the living dead to continue functioning…

By driving interest rates to zero savers have been robbed of interest on deposits while that income has been transferred to the debtors essentially the insolvent fiat banking system, and so the last ten years has been a slow motion wealth transfer from the productive to the unproductive which has only made these zombies more dependent on cheap money and low debt service costs, and has only made them weaker when interest rates start rising again (as they are now) as the tide goes out on the next credit crisis the financial sector will be far more naked and exposed than ten years ago…

2s/10s yield curve – a popular measure of net interest margins (credit spreads)

Another by-product of a decade of Zero Interest Rate Policy was the compression of the bankers profit margins on money, otherwise known as Net Interest Margins or the margin between short term borrowing and long term lending, manifested most popularly by the 2S 10S Yield Curve and the spread between two year and ten year debt (US Treasury), and is currently at the lowest since before the last crisis, and with yield curves in corporate debt markets heading the same way the flatter the yield curve the lower the profitability of money, and thus the profitability of a crucial component of modern banking… When the yield curve inverts is when short term debt and interest yields more than longer dated (and riskier) debt and is an abnormality created by interest rate setting and meddling central bank policy… As I commented in my original post the irony of this central bank low interest regime is to weaken and poison the children in commercial and retail banking, the only reason that central banks exist lest we forget, is as the backstop for these high street banks… In the last crisis it was Central Banks that bailed out the private banking sector, the next crisis will require the bailouts or restructuring of the Central Banks themselves…

Removing the profitability of money and the compressing of margin spreads on interest yields and loans forces the banks to rely on other sources of future revenues, of which the other major source is trading revenues… By running and rigging exchanges and Wall Street Casinos, whether their clients and fund managers win or lose is irrelevant to them as they make money and commissions on the trades themselves, so a bankers wet dream would ideally be volatile markets but alas for that the markets would have to be un-rigged and that is impossible in a centrally planned world, and so in the name of “stability” of the financial system in the wake of 2008 the Central Bank put in goosing the value of stocks and bonds has crucified the hedge fund industry as hedging is now obsolete, capital has shifted from Active Investing (Hedge Fund Managers) to Passive Investing (ETF’s, stock indexes) and High Frequency Trading, measures and hedges of volatility such as precious metals and the VIX (Volatility Index) have been rigged to within an inch of their lives as the low volume Regime ground asset values higher for what has felt like aeons… With the interest rate hikes instigated since 2016 by The Federal Reserve having yet to seep into the longer end of yield curves and boost bank profitability, what hiking the Federal Funds Rate has accomplished so far is increasing the debt service costs of a debt based economy addicted to low interest rates, that will manifest in the next crisis most likely as a corporate credit crisis that will halt the financing of stock buybacks that has been the main gooser of this last decade long stock market boom, mortgage rates rising is triggering the next housing bust and with debt service costs generally exploding everywhere it is self evidently bearish for asset prices, and bearish for the banks and central banks who are the ultimate holders of all this debt that been issued the last decade and which will have to be one way or another, sooner or later, be marked to market… I don’t think hardly anyone realises and understands just how unprecedented and damaging zero interest rates have been for the West, and how fragile the whole financial system becomes at the slightest uptick in what have been the lowest interest rates in the last five thousand years… A snake eating its own tail…

So with the prospects grim for the banking system in interest margins, increasing debt service costs across the board and popping stock, bond and housing bubbles, where were the revenues going to come from to keep the banking and by extension financial industry afloat in the medium and long term? I argued in my original post that the banks (and the central bank that exists for the survival of the banks, do not forget) would open up their ledgers and profit opportunities to the Bitcoin Network, and like most of my futurist writing was wildly optimistic and premature, however the simple truth then as now is that Bitcoin specifically (and the crypto/shitcoin space more generally) will give banks an extended lifeline in keeping them alive in the short, medium and long run, which I will get into far more detail later on… Bitcoin and banking are distinct and completely separate ledgers and currency systems and therefore can only connect at exchange points, and as the wealth (in the form of future liabilities, or debt) is currently trapped and being levitated by central bank ledgers, currencies and derivatives, then it is also banks that have to allow the access for the wealth to travel off their ledgers and currencies and into Bitcoin’s ledger and currency… For building the bridges that allow two distinct ecosystems to connect, the banking system gets to charge the fees and tolls for the wealth crossing over, and allows it to regulate the exchange (choke) points between banking and Bitcoin, which is really at the heart of this post too… The price these banks will have to pay for the milking of Bitcoin exchanges is in feeding their nemesis and ultimate destroyer, as the shrinking of one monetary bubble inflates another monetary bubble, and that once the wealth was contained within Bitcoin that would be the end of the bankers control over that wealth… Bitcoin cannot be controlled or regulated by Banks or Governments in any way whatsoever, save through the gateways that connect both ledgers and networks…

Bitcoin Kills Banking Revisited – Regulating Bitcoin

My Bitcoin Kills Banking Revisited Post of June 2017 discussed many topics but I will concentrate here on this question of regulation, not just of Bitcoin but of the whole crypto space in general and how this regulation would vary between regions and countries, as we have not quite yet become a One World Government New World Order… In my post I explained that regulation would vary from Country to Country dependent on many factors including how threatened governments would feel and therefore react to it, their level of understanding, the electricity and internet infrastructure, laptop and smartphone adoption rates and tech literacy of the public in general, and how corrupt and despotic the rule… And in my post I naively and really blindly predicted that Western Governments would clamp down and more tightly regulate Bitcoin exchanges and that Eastern Governments would be the ones to lightly regulate Bitcoin exchanges, within a few months the Chinese Communists had severely clamped down on their mainstream exchanges making a mockery of some of my predictions, while in the time since it is the US that is now actively developing regulations to work with Bitcoin and is far ahead of the UK and the EU in this respect… The last eighteenth months hasn’t panned out quite as I’d expected, and for the US, a lot of that is down to Donald Trump…

A section of the post further discussed the pros and cons of Bitcoin regulation, because there is a world of difference in how Bitcoin markets develop in relation to government interference… For example the benefits of banning Bitcoin outright is a stemming of fiat leakage (at least directly) by shutting off the online exchange method, which would force traders to the shadow and dark markets of peer to peer over the counter exchange whether through individual bank account transfers or through physical cash, which directly leads to the disadvantages of clamping down on Bitcoin, you lose all control over the exchanges you force underground, you cannot any longer regulate exchanges, you cannot collect fees for exchanges, you cannot tax exchanges and you cannot effectively surveil exchanges, so while in the short run governments and banking systems could largely tamp down on the network effects of Bitcoin by deciding to have nothing to do with it, they also lose access to taxation and snooping that would provide bankrupt governments the world over with a steady source of revenue and shakedowns…

While the obvious disadvantage of lightly regulating Bitcoin exchanges is fully embracing the monetary system that will make you obsolete and thus drain all your wealth and power in the long run, in the short run you get fees, you get taxes, you get to regulate exchanges to your own benefit, to a certain extent get to surveil and track the flows from Fiat into Bitcoin exchanges, can potentially track onto Bitcoin’s public blockchain from exchanges, and you can fund budgets for regulators and law enforcement… As desirable at it would first appear to outlaw Bitcoin for threatened banks and government regulators, there is the counter-strategy of seeking to control and co-opt Bitcoin through government and fiat regulation, and even gives the opportunity at these centralized exchange points to manipulate and rig the price, like they have done with gold, silver, virtually all commodities, stocks and bonds… Where there is the opportunity to exchange and set prices there is also the opportunity to manipulate exchange and rig prices, and is always a double edged sword…

My original call for China and the East to adopt crypto-currencies while it would be shunned by the West as Petrodollar and SWIFT competitor has been largely disproven at least for now, while Japan and South Korea have developed what many would call a light touch regulatory structure, China clamped down on all its major and liquid online exchanges which has exploded the over the counter peer to peer market in China through exchanges such as Local Bitcoins and through mobile phone apps such as Alipay, which has also meant that the Chinese Communists have to a large extent lost control over the exchange of Bitcoin in their own country, at least until they decide to relax and lighten their regulatory outlook… The EU and the UK have also been indifferent or even hostile to working with Bitcoin exchanges, and so this leaves us with the case of United States regulation of which I have paid most attention to over the last few years, as I believe that the US is the most developed with regards to fully regulating the grey area whence the Dollar and Bitcoin connect, of which more later…

Bitcoin Kills Banking Redux: Exchanging And Exchanges

This third and last post of the banking trilogy will concentrate on exchanging and exchanges, and in trying to elaborate on what exactly constitutes an exchange, how exchanges differ and will differ in light of increasing regulation in connecting to the banking system, in all this will be a pretty long and expansive post in of itself just discussing exchange…

The first question is what constitutes an exchange, and to provide a relatively detailed answer I need to split exchanges into prototypes, as follows:

Exchange Prototype 1: Decentralised Exchanges (DEX’es)

Exchange Prototype 2: Smartphone (Cash) Apps

Exchange Prototype 3: Centralized Exchanges

Exchange Prototype 4: Fiat Derivatives (Cash settled futures, ETF’s, etc)

Exchange Prototype 5: Banking Protocols (Ripple XRP, Stellar Lumens)

Exchange Prototype 6: Stablecoins (Tether, USD Circle, JPM Coin, etc)

Before I get into discussing these categories in more detail, I feel it would be instructive to give a brief background of the history of Bitcoin exchanges developed to today, to give greater context to the present and therefore the likely future development of exchanges…

A Brief History of Bitcoin Exchanges

Bitcoin was launched in the first few days of 2009 in the whirlwind of the 2008 financial crisis, as Satoshi released the code from scratch, ran the miners and nurtured the network until his disappearance, there was as such virtually no exchange built to allow anyone other than a Bitcoin miner to own bitcoins… The first exchange of any note in those early years was Mt Gox (launched July 2010) that allowed both miners to sell their bitcoins for fiat and for outside retail investors to sell fiat to own bitcoins, and therefore it became the premier price discovery point of Bitcoin’s early value in fiat currencies… Other notable early exchanges were Bitstamp launched August 2011, Local Bitcoins (an over the counter peer to peer exchange) launched June 2012, Coinbase launched October 2012 and Bitfinex launched December 2012, but for those early years Mount Gox ruled the price of Bitcoin as the most liquid exchange and traded at over 70% of Bitcoin transactions worldwide going into its demise… The early, crude, fragile and ultimately bankrupt Mt Gox and its teetering underlying accounting infrastructure as really the first major and completely unregulated exchange, contributed heavily to Bitcoin’s parabolic bull market of late 2013 and the bear market of 2014 and 2015 in the wake of the bankruptcy of Mt Gox in February 2014, indeed the near five year long legal fight for the rumoured 200,000 bitcoins trapped in the rubble of Mt Gox has haunted Bitcoin ever since… However it is unlikely if Bitcoin had have developed to its scale of today without the early infusions of fiat that attracted hodlers and developers and new exchanges in competition… As bitter as some Bitcoiners may feel towards Mt Gox and Mark Karpeles, imagine what things could be like if it never existed?

Following the collapse of Gox in Japan exchange was then increasingly divided between Chinese (mostly zero fee liquid and centralized exchanges) and as regulatory developments proceeded in the US particularly lead to the rise of Coinbase, Kraken (launched September 2013), Gemini in 2014 to name a few of the prominent American exchanges… As China and Bitmain came to dominate Bitcoin mining from its first halvening in 2012 then it was natural that Chinese exchanges would flourish in selling these bitcoins in the open market, at least until the Chinese government decided to outlaw them, since 2017 and the fight for SegWit which Bitmain lost, China’s exchanges and mining has diminished in influence and it is currently Japan, South Korea and the US I would deem most open to working with Bitcoin at the moment, with the EU, UK, and China with far less legal and regulatory clarity…

To briefly conclude, the last ten years despite numerous hacks and blowups of early Bitcoin exchanges as a completely new asset class was highly centralized and subject to fiat fragility, since the collapse of Mt Gox Bitcoin exchange has flourished in both centralised and regulated exchanges and in over the counter unregulated and decentralised exchanges, and spans I would imagine nearly all of the world’s two hundred countries, numbering in the hundreds and operating on four continents… Where Bitcoin to fiat exchanges in the early days were few, centralised and inherently fragile, they are now spread out over continents and nation states, distributed, decentraliaed and inherently anti-fragile, and in my opinion it is highly unlikely that nation states could ever come together on a global scale with uniform Bitcoin regulation, rather the extent of regulation applied across countries will drive adoption of Bitcoin in different ways and to different degrees… For this is the essential truth of Bitcoin exchanges, they are only a mirror of the willingness of national regulators and the banks that lobby and direct them in working with Bitcoin, early Bitcoin exchanges were slow to develop because of a lack of any national regulation for Bitcoin, therefore banks were extremely cautious (especially in the wake of the 2008 financial crisis) in dealing with crypto-currencies because of money laundering connotations, crime, drugs, and all the uncertainty surrounding this most mysterious of creations… The last decade has been the development of regulations in line with the desires of national banking systems as regards Bitcoin, and they are more developed than ever in every nation on earth today, and I feel another worldwide banking crisis magnitudes worse than the 2008 calamity will only speed up this national regulation and so we will have to see how this develops in the Americas, Europe, Africa, and Asia…

Exchange Prototype 1 – Decentralised Exchanges (DEX)

“Decentralised” could be argued is a broad term but covers what I would call peer to peer trade or over the counter trade, which would encompass both online trading through direct bank exchanges, face to face through cash and also I would deem includes brick and mortar businesses and ATM’s (Automatic Teller Machines)… The earliest prototype of this method of exchange was LocalBitcoins launched in June 2012 as an over the counter exchange, with no centralized exchange as such but a direct exchange of online fiat bank transfer for bitcoins (which they also taxed you for not removing offline to cold storage), also LocalBitcoins allowed for face to face exchanges and clearance and the creation of local physical markets, in my opinion like Mt Gox the Bitcoin community owes a big debt of gratitude to LB for allowing early adopters access into a relatively convenient and private method of procuring bitcoins… Even so, in light of a recent case where a trader was reportedly (from Reddit) shaken down for an ID there have been rumours (unconfirmed by Local Bitcoins AFAIK) that the exchange may adopt KYC/AML (Know Your Customer/Anti Money Laundering) regulations under pressure from national regulators and banks no doubt, by tying your bitcoins to your identity LB would shift from a decentralized online exchange (although over the counter and peer to peer) to centralized in nature… Further examples of non KYC/AML decentralised exchanges include Paxful and HodlHodl…

A great example of what I consider a real decentralised exchange is Bisq.Network launched April 2016, and is different from virtually any other exchange that I know of in that it’s a protocol with an in built client, a software download and connection over Tor (and anonymous onion routed networks) that allows users to buy and sell bitcoins (and many other currency pairs) through dollars, euros, pounds or yen, but there is no central repository for funds, thus direct and peer to peer anonymous bank transfers for bitcoins make it virtually impossible to tie identity to bitcoins… Bisq is my envisioning of a DAO (a Decentralized Autonomous Organisation) that is a corporation without owners but merely contributors, a public utility more than a private entity, and thus by its nature uncensorable and cannot be regulated either… For these reasons among the more libertarian and paranoid Bitcoiners there is an anonymous method of HODLing and so these exchanges will always exist, and will likely flourish as the demand for DAO’s in many applications of finance and law will continue to be built on top of the Bitcoin triple entry-bookkeeping ledger and accounting system… If you are looking to purchase your bitcoins as privately as possible then I would suggest you download Bisq and give it a try…

The other method worthy of further discussion is Bitcoin brick and mortar premises and dealers (a corollary to the precious metals coin dealer) and physical ATM’s also provide a face to face and “private” method of exchange, but obviously dependent upon surveillance and KYC/AML regulations that are yet to be fully developed by national governments, up to December 2018 there are now over four thousand Bitcoin ATM’s worldwide and another four thousand price discovery points at the gateways between fiat currencies and bitcoins, and with over seventy percent of these ATM’s in North America either by technical ingenuity or more defined US government regulation, Bitcoin exchange at the local level is flourishing in the US… I expect further expansion in this sector as with all other sectors, with a failing Banking system and a decade long booming Bitcoin ecosystem I also expect this (low key so far) brick and mortar Bitcoin buyer and seller to explode and proliferate in high streets all over the world, as a familiar face and experienced know how in how to buy and store bitcoins would be an additional benefit and service to un-knowleadgable and inexperienced newbies entering Bitcoin, so a shop also doubling up as an educational centre in my opinion is at the heart of long term Bitcoin adoption, depending on how Bitcoin is regulated from now on… If Bitcoin is given legitimacy and were money laundering and money transmitting laws and regulations to be relaxed, then Bitcoin dealers and traders could establish high street premises and pay taxes on earnings, whereas a clamping down on either brick and mortar premises or ATM’s would drive these honest entrepreneurs to the dark markets of anonymous cash transfers on street corners, and of which national governments could only hope to track, surveil or tax…

In conclusion, Decentralised Exchanges will always exist for those who seek privacy and anonymity in their Bitcoin dealings, these are over the counter and peer to peer markets and they require more homework to use than more fashionable centralised exchanges and smart phone interfaces of exchanges such as Coinbase… As these markets are peer to peer they are also (compared to centralised exchanges) illiquid and therefore they will typically carry a price premium to more liquid exchanges, the price you must pay for privacy and anonymity is higher than you would pay for a fully regulated liquid exchange, and while the cost of a software download like Bisq is zero, Bitcoin ATM’s and physical premises cost rent, the machines cost money, dealer time and expertise cost money, so these will likely carry a significant premium to the convenience and liquidity of regulated and centralised exchanges… The decentralised exchange exists for the individual and retail investor it is mostly or completely unregulated and virtually impossible to shut down, but it should be clear that institutional (read Wall Street) money will never choose this method to get into Bitcoin as they require clear and defined regulation, it should also be clear that beyond regulated exchange points there is the unregulated and private market for Bitcoin, and these two will continue in parallel and independent of each other…

Exchange Prototype 2 – Smartphone App Exchanges

While at first glance smartphone/device apps such as Coinbase, Square and Robinhood may look decentralised for the retail (individual) Bitcoin user, I consider two distinctions that make these cash apps centralised and cognate with centralised exchanges, in that they have custodial control of the bitcoins and that they require KYC/AML linking of identity to Bitcoin purchases, for these reasons I would not consider these peer to peer exchanges…

The benefit of these apps is that they are in both Apple and Google Play Stores and a few seconds download away from you being able to buy Bitcoin, they are also highly convenient due to corporate User Interfaces with one or two click buying or selling which cuts out many of the hurdles that the necessity of privacy and illiquidity automatically applies to Decentralised Exchanges (as discussed above), but to be clear the trade-off for retail convenience is registering and linking bank account or payment processor to the exchange and therefore creating a potential (centralized) honeypot for government tax shakedowns, the price of convenience is corporate and governmental surveillance…

As these apps have by design been approved by regulating bodies and implicitly by the banking system, I also expect these smartphone apps to proliferate and to target inexperienced newbies to the Bitcoin space with convenience in exchange for surveillance capabilities, but with the allowance for redeeming Bitcoin onto the main chain even though this is an effective honeypot for taxation and money laundering shakedowns and prosecutions, if Bitcoin is removed by users and stored off of these exchanges, this is a far more frictionless method of accumulating and trading bitcoins and will I’m sure largely appeal to the retail class…

In conclusion I consider Bitcoin smartphone apps as another retail method for Bitcoin ownership but in a more centralised manner than decentralised exchanges, as these companies are still central repositories of Bitcoin and as such are security holes and honeypots for hackers… However they are also convenient for newbies as a quick method to start accumulating Bitcoin, by their very nature have government and banking licences and are highly regulated which should mitigate investor losses by giving them consumer protections, in exchange of course for KYC/AML registration and surveillance for money laundering and taxation purposes… They also and most importantly in my opinion allow the withdrawal of Bitcoin off their exchanges and onto the main chain for offline storage in hardware wallets… Smartphone apps allowing exchange between fiat and Bitcoin will I believe continue to develop unless the banking or governmental regulations changes to a far more hostile environment (which I can easily envisage as Bitcoin grows in threat to dying fiat money and banks), or unless there is either a very stringent IRS tax shakedown or some sort of cyber hack resulting in the theft of and/or run on the exchange, but this would merely bring to the fore the more fragile nature of smartphone apps and exchanges… Their business model is far more dependent upon banking and regulatory relationship than decentralised exchanges and so this balance is inherently and intriguingly dependent upon continued regulation compliance… The more light touch regulation and less banking compliance is required the more I would expect most retail adopters to use smartphone apps even with all the surveillance it entails, because of the convenience of linking these apps to credit cards or bank accounts, while increasing regulation and compliance and heavy handed taxation enforcement or banking clampdowns to stem the flow of fiat into these smartphone exchanges, would see the retail user flood into the far more anti-fragile if inconvenient decentralised exchanges while these centralised exchanges wither… Decentralised retail exchanges will and do exist all over the world regardless of banking and governmental regulations, centralised smartphone apps will proliferate according to national banking and governmental regulations and will therefore vary depending upon each nation’s legal and regulatory structures…

Exchange Prototype 3 – Centralised Exchanges (Institutional Gateways)

Decentralised exchanges and smartphone apps are a relatively new phenomenon that allows the retail user an insane amount of easy and less easy options of getting into Bitcoin, however in the early days the old fashioned way of getting bitcoins (outside of mining) was by an exchange such as Mount Gox as I have already discussed, but the nature of these exchanges due to the complete lack of any regulations with banks or governments was a wild west of fragile monopolies prone to fractional reserves and eventual blow up… The exchanges since Gox have become far more professional and in general less prone to hacks because of learning of mistakes, increased security, and maturing of the exchange and developers, and this has happened in lock-step within an increasingly defined banking and regulatory legal framework, and while these third parties are still obvious security holes and honeypots for exchange hacks (and loss of user funds), increasing regulation should work to minimise and shore up losses, because this opens up a hitherto astronomical untapped market of fiat money, that is institutional investment and the wolves of Wall Street… I believe there is a secular shift underway in the realm of the centralised exchange, and of the first generation of Bitcoin exchanges from retail to institutional… The most successful of the early exchanges that flourished in the wake of Gox are I believe in the process of moving away from individual trading and retail accounts toward Wall Street and institutional investors but only of course when the regulatory hurdles that prohibit Wall Street from investing in Bitcoin, are cleared… We have seen Coinbase move toward regulation by the SEC as a Registered Broker Dealer for expansion into institutional markets, they have secured a New York State Bank Charter as an independent Qualified Custodian in the last few months, and is in the process of integrating its platform with Fidelity (one of the world’s biggest retail brokerages), so it should be coming clearer that while Coinbase still serves the average retail investor (at least for now), it is looking for bigger fish to fry… I expect a few of these first generation exchanges to pivot from retail investors and Billions in trade toward institutional investors and Trillions in trade and likely millions or billions in fees, raising the barriers to entry to encourage institutions and to discourage retail investors, who do have many other options as I’ve discussed above… Coinbase would be under heavy competition from the aforementioned cash apps in the future anyhow, while they should be considered somewhat of a pioneer in creating the institutional and second generation of Bitcoin exchange, and where there is by definition, less if any competition… From Main Street to Wall Street…

In discussing further this institutional investing, first we need to briefly examine current regulations and consider how Bitcoin is currently defined and by who, and here I will concentrate exclusively on the U.S because even though Bitcoin is now a decade old, most national governments and banking systems still have not developed a comprehensive and over-arching regulatory framework, and possibly outside of Japan (who’s regulatory structure I’m not that familiar with) the U.S. is by far the most developed, which is just another way of saying that the U.S. (backed by its banks who lobby its regulators) have decided at this point at least that they are willing to allow mainstream fiat institutional investing… In 2015 the CFTC (Commodities Futures Trading Commissioning) declared that Bitcoin would be regulated as a commodity (like gold, silver are commodities), and to date no other altcoin (despite Ethereum rumblings) have been added as commodities, they are rather under the purview of and regulated by the SEC (Securities And Exchange Commission), so straight away a distinction must be made between Bitcoin and all other altcoins… U.S regulators have figured out that Bitcoin is a leaderless bottom up regulated protocol and its currency has to be regulated as such (a commodity), while virtually all other alternative coins are top down centralised rivals in leadered blockchains, and as such in my opinion must be regulated as securities (including Ethereum)… I really do not see how Ethereum or any other coin (outside of possibly Litecoin) can with an authoritarian and publicly visible developer team possibly escape securities regulation, and as I discussed at length in my post on Ethereum of a year ago, this gives Bitcoin a regulatory privilege in the US that likely makes impossible for any alternative to compete with… In a sort of delicious irony it is likely in fact that no alternative coin or project will rival Bitcoin because of its regulatory status and its first mover advantage in the world’s most financialized economy, and it will be government regulators that will clamp down on any competition to Bitcoin in the world of physical trade and derivatives exchange (and which I’ll discuss in more detail later)…

So the obvious question: why would institutions want to invest in Bitcoin?

My answer: many reasons… In my banking posts I have discussed banks and central banks holding Bitcoin as a hedge (in the same way as they hold reserves of gold) against the inherent loss of purchasing power of their own fiat currencies as they print them into oblivion, I have discussed Bitcoin as a pipeline for banks and national governments in by-passing financial sanctions and evading central monopolies such as the Petrodollar and SWIFT, and I have discussed Bitcoin as a long term store of value digital bearer asset for retail investors (hodlers) that also naturally applies to institutions and outside of merely banks, this includes pension funds, insurance funds, hedge funds, exchange traded funds, in fact any and all other financial and regulated fiat funds… As I described in my original banking blog, the post 2008 years of Zero Interest Rate Policy that hath ruled for the last decade has made the fiat money system increasingly unprofitable not just for banks, but for the whole financial industry in general, if you even casually browse under the thin veneer of today’s mainstream financial cheerleading, profitable hedge funds are an increasingly extinct breed while the central bank put has made hedging and volatility extinct, and while stocks are at near record highs while government, corporate and municipal bond (debt) yields are at all time lows, there is a limit to stock buy backs and and bond yield suppression, and that is central bank expansion of credit and liquidity… This central bank liquidity is centered around the Federal Reserve System as World Reserve Currency since 2015 has been a glacial regime of Federal Funds Rate hikes at the short end, and Quantitative Tightening at the long end to slowly increase interest rates and the cost of debt and debt service all the while draining base money out of the system, while also to a certain extent forcing other banks around the world (Bank of England, European Central Bank, The People’s Bank of China and the Bank of Japan in particular) to start tightening themselves and which is contributing to a slowing globalist economy, and to rising volatility and stock and bond selloffs… We are likely past the point of maximum extension (despite China still printing TRILLIONS) in this latest and in my opinion the last credit boom and bust cycle and this one has been particularly epic, over a decade in length… While hedge funds may become reinvigorated by the imminent recession and great credit meltdown of this year and next when hedging will start paying off again, pension funds and insurance funds heavily invested in stocks and bonds will suffer catastrophic losses as debt and leverage of a criminally underfunded ponzi scheme turns sour again, it is my contention that to save themselves in the short and the long term, to save the investments of the millions of people dependent on pension, insurance and corporate payouts, the whole investment world built upon debt will have to pivot away from debt and into sovereign and non debt assets, such as physical gold and “physical” bitcoin…

As I discussed in my second banking post in 2017 one of the biggest worldwide trends to watch over 2017 and 2018 was the regulation of Bitcoin exchange by the world’s insolvent banks and governments, because this institutional investing cannot reach anywhere close to its potential without fully regulated methods and means of investing, and that the need to create these regulatory frameworks would become more urgent the closer we came to the next financial crisis… At the start of 2019 the seeds of the next crisis have long been sown and I believe that institutional regulation of Bitcoin exchange is far more developed in both the US and Japan than in the EU, the UK, and the rest of the world (with a few exceptions in tax havens), so I believe that institutional investing in Bitcoin will begin on Wall Street through its banks (which have co-incidentally bought into directly or indirectly a few of the first generation Bitcoin and Shitcoin exchanges), you have Coinbase and Gemini‘s moves toward New York regulation and Licences for this very eventuality… The one major ongoing obstacle to direct ownership of the underlying asset (Bitcoin) is the so-called Custodial Solution, i.e a critical component of institutional regulation is storage issues, and usually requires a centralized and fully regulated custodian which amusingly is the complete antithesis of the principle of Bitcoin that ownership does not require a counter-party and therefore is a self custodial asset, these institutions seeking to invest in Bitcoin could get bullet proof custodianship for a few hundred dollars with a simple hardware wallet, however this will not be the case within the Fiat system and so a decentralised asset must be centrally stored and secured… This custodial solution that unleashes hedge funds, pension funds, and all sort of manner of other funds into Bitcoin ownership is apparently on our thresholds right now, which brings me to the Bakkt Exchange and what I believe is the most advanced prototype of what a Bitcoin institutional exchange will look like… Bakkt we need to discuss in some more detail…

Bakkt Exchange – Second Generation Exchange

I will begin with what initially pricked up my ears, and that is who owns this exchange, and quoting from this Business Wire article,

“ATLANTA & NEW YORK–(BUSINESS WIRE)–Intercontinental Exchange (NYSE:ICE), a leading operator of global exchanges, clearing houses, data and listings services, announced today that it plans to form a new company, Bakkt, which intends to leverage Microsoft cloud solutions to create an open and regulated, global ecosystem for digital assets. The new company is working with a marquee group of organizations including BCG, Microsoft, Starbucks, and others, to create an integrated platform that enables consumers and institutions to buy, sell, store and spend digital assets on a seamless global network.”

Owned by an established and experienced exchange operator, working with some of the more successful corporations in the US today, so very interesting… Some more on Intercontinental Exchange, owner of Bakks, quoted from the same article…

“About Intercontinental Exchange

Intercontinental Exchange (NYSE: ICE) is a Fortune 500 and Fortune Future 50 company formed in the year 2000 to modernize markets. ICE serves customers by operating the exchanges, clearing houses and information services they rely upon to invest, trade and manage risk across global financial and commodity markets. A leader in market data, ICE Data Services serves the information and connectivity needs across virtually all asset classes. ICE is the parent company of the New York Stock Exchange, which has helped companies raise more capital than any other exchange in the world, driving economic growth and transforming markets.“

Some further discussion on regulations…

“The Bakkt ecosystem is expected to include federally regulated markets and warehousing along with merchant and consumer applications. Its first use cases will be for trading and conversion of Bitcoin versus fiat currencies, as Bitcoin is today the most liquid digital currency. The effort is designed to address evolving needs in the estimated $270 billion digital asset marketplace.

Applications for digital currencies continue to develop alongside regulatory frameworks and rising investment in blockchain technology which, halfway through 2018, has already exceeded all of 2017, according to KPMG. By leveraging trusted market infrastructure, Bakkt is being engineered to help the digital asset markets evolve securely and efficiently while supporting transaction flows.

“In bringing regulated, connected infrastructure together with institutional and consumer applications for digital assets, we aim to build confidence in the asset class on a global scale, consistent with our track record of bringing transparency and trust to previously unregulated markets,” said Jeffrey C. Sprecher, Founder, Chairman and CEO of Intercontinental Exchange.”

And finally from the same article, some more on the products that Bakkt is likely to offer…

“As an initial component of the Bakkt offering, Intercontinental Exchange’s U.S.-based futures exchange and clearing house plan to launch a 1-day physically delivered Bitcoin contract along with physical warehousing in November 2018, subject to CFTC review and approval. These regulated venues will establish new protocols for managing the specific security and settlement requirements of digital currencies. In addition, the clearing house plans to create a separate guarantee fund that will be funded by Bakkt.

“Bakkt is designed to serve as a scalable on-ramp for institutional, merchant and consumer participation in digital assets by promoting greater efficiency, security and utility,” said Kelly Loeffler, CEO of Bakkt. “We are collaborating to build an open platform that helps unlock the transformative potential of digital assets across global markets and commerce.”

I will include a further snippet from another good article, relating to institutional investing…

“Institutional Investment

The first is the obvious nod toward institutional investment. Bakkt has that covered with its initial slate of venture capital firms. If these firms are willing to stick their necks into the crypto arena, so the thinking goes, it’s just a hop-skip-jump for even larger firms to come onboard. This is particularly likely if Bakkt plays by the regulatory rules and secures approval for its operations moving forward.

Oddly, this argument also works in reverse. If big-ticket investors are fine with Bakkt’s operations, then it follows that small-time investors should come on-board, as well. It’s a known fact in the financial world that little money follows big money, the way little fish trail bigger fish to feed on scraps. If a large venture capital firm is confident in Bakkt, the firms that look to it for guidance will follow suit. This has the potential to bring in a slew of capital from previously untouched resources — credit unions, retirement accounts, and 401(k)s. By nature, these types of holdings need to be conservative. They exist, after all, to help investors prepare for the future. Without significant institutional backers, the crypto market has been famously volatile. In kind of a vicious circle, that lack of institutional money due to volatility has prevented an injection of capital which could keep volatility to a minimum. It’s obvious, then, that Bakkt’s entry into the market can only calm the fears of naturally conservative investment vehicles.“

Current Status of Bakkt – Awaiting Regulatory Approval

The current status of Bakkt, like much of the development in this nascent second generational exchange space brings us back to a central theme of this post, that of regulation… Depending on your view of regulatory bodies like the CFTC and SEC either in the context of Wall Street gangster enforcers against competition, or as defenders of consumers and institutions under US Law, when considering the TRILLIONS upon TRILLIONS of dollars that could flow into Bitcoin and its exchanges, this regulation may take some time (Bakkt is already delayed by a few months) to iron out and in the minds of regulators to get this as “right” as possible, the Bitcoin shills who evangelise the embrace of Bitcoin by Wall Street to pump up the price may have to wait another 12-24 months for this to even begin, however as I have also already discussed we are at the early stages of the next financial crisis that will force banks, institutions as well as consumers into buying Bitcoin as a hedge against the latest collapse of Fiat, and as the regulators are essentially the enforcers of Wall Street lobbyists and bankers, I do expect these regulations to be sorted only for the reason that it will be in Wall Street’s interest to do so… Tick, tick, tick…

Exchange Prototype 4: Fiat Derivatives Exchanges

If the premise of the Bakkt Exchange is the settling of physical (so to speak) Bitcoin or the buying and selling of the underlying asset on Bitcoin’s sovereign blockchain (ledger), the premise of Fiat derivatives are trading without the underlying asset, a purely fiat exchange pegged to the underlying price of Bitcoin on primary fiat exchanges… This may sound like a negligible distinction but it is far from it, while the first scheduled asset of Bakkt is a physically secured and delivered Bitcoin contract, in the last year both Comex (Chicago Commodities Exchange) of the CME (Chicago Mercantile Exchange) and the CBOE (Chigaco Board Options Exchange) have already launched cash settled Bitcoin futures, and while fully regulated by the CFTC it should be clear that there is no trading of Bitcoin in any physical form but only a fiat claim upon the Bitcoin price (for the CBOE, futures prices are tracking the value of bitcoin in $ on the Gemini exchange)…

Futures Exchanges

bitcoins first day – @JimBTC’s hilarious take on the chaotic CBOE Futures launch of 10th December 2017! (source)

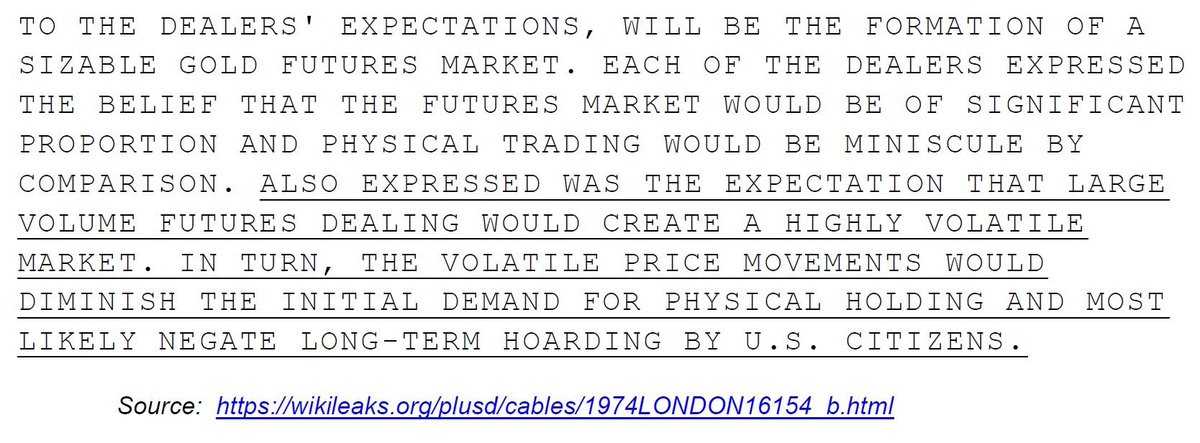

Indeed the launch of cash settled futures late in December 2017 co-incided with the manic driven peak of Bitcoin at the cycle high of around $20,000, the year since the price of Bitcoin has collapsed some 80% and this Correlation Is Causation event has brought out all the schadenfreude of the hard money gold bugs, in proclaiming that the price of Bitcoin is now rigged in exactly the same way as physical gold prices were rigged following the end of the Gold Standard in 1971…

Wikileaks 1974 Cable Reveals Purpose of Creation of Gold Futures Market (H/T Smaulgld)

As much as it may provide comfort to gold bugs in believing this fable that cash settled futures is the death of Bitcoin, I must point out some rather fundamental and obvious differences between gold and Bitcoin as commodities… Gold in human history has always been money but its major drawback is that it is an inert metal that has never had a credit settlement layer, indeed gold as an inert metal was the historical foundation for credit ledgers and currencies to be built on top, therefore the history of gold and banking are eternally inter-twined and to this day the main goal of central banking and the rigged fractionally reserved gold exchanges at the Comex, the LBMA and the SGE (the three main setters of the price of gold set in Dollars, Pounds and Yuan), is to manage the price of gold to give the insolvent fiat system the thinnest of veneers of respectability… What the banks have been able to do with gold is rig the overlying ledger and credit apparatus to marginalize and discredit the underlying commodity and the historical role of gold so they do not have to return to a gold standard, and so far at least, so good for the bankers…

Bitcoin on the other hand is a digital commodity with its own credit settlement ledger and is therefore fundamentally different from gold, and to be clear ownership of bitcoin can only be accounted for on Bitcoin’s ledger and not on any other ledger, while this does not preclude fiat money from manipulating the price of Bitcoin in the short or medium term (with exchanges being the primary (choke) points of price manipulation), in the long term the boom and bust bubble machine of central banks and fiat money cannot control the Bitcoin ledger or effect in anyway upon its monetary policy which is hard-coded, the only place that fiat can regulate and rig is the connection between ledgers, the fiat ledgers and the Bitcoin ledger… And unlike the private and highly secretive ledgers that the bankers who ruled the world have been able to build on top of gold to flip the monkey into the organ grinder, the Bitcoin ledger is a public and pseudonymous online ledger that anyone can connect to entirely by-passing banks and goverments, and thus Bitcoin holds the fraud inherent in fractional reserve banking in check in a way that gold has always been unable to, and brings up another point of how far banks can rig the Bitcoin price downwards over time… Unlike the gold market that has been completely de-monetized (From 1934 when FDR banned gold ownership) and is strictly controlled on the margins by the merciless rigging of the gold price utlising three main gold futures exchanges, Bitcoin has no connection or history to the fiat system and is in fact monetising, it has gone from zero to $4,000 and a $70 Billion market cap in only ten years, and is as I have described in my past banking posts slowly emptying the fiat system of its wealth… Every day it survives Bitcoin as a network gets stronger and anti-fragile and every day the fiat money ponzi scheme becomes more and more over-levered and fragile, while it is possible for the fiat system through cash settled derivatives to manipulate the exchange rate of the underlying bitcoins, the trend will be toward consumer and institutional ownership of the underlying asset, that as a reminder would be as a hedge against the loss of trust and purchasing power of fiat currencies and derivatives, renders the derivative worthless… The flood to Bitcoin with a maximum cap of 21,000,000 and a daily issue rate of 1,800 cannot be hypothecated or re-hypothecated, completely by-passing rigged and fractional derivatives of a counter-parties claim… Rigging Bitcoin and rigging gold are two entirely things…

The positive developments that cash settled futures have enabled is for hoarders of bitcoins (which at this stage of development is still volatile) to hedge by taking out futures contracts denominated in fiat money, this allows Bitcoin miners for example to hedge Bitcoin’s price volatility with fiat stability as miners are somewhat of a hybrid, they work to produce bitcoin but their running costs in terms of capital hardware are electricity costs will be denominated and payable in fiat money, thus buying or selling cash settled futures can help lock in some profits or mitigate losses, much in the same way as other commodity producers in oil and other markets use futures contracts to the same end… Cash settled futures that are nearly exclusively in the US for now I expect will develop in other countries and markets in order to stabilize bitcoin businesses and companies while we slowly transition from banking to Bitcoin, and is but another example of the connecting of legacy monetary systems with an emerging monetary standard… Anyone who tells you that cash settled futures are worthless or a ponzi scheme is wrong…

ETF (Exchange Traded Funds) – Retail And Institutional Investing

Another long saga that has been hailed by Bitcoin shills as the re-birth of the 2017 parabolic bull market is the final granting by the Securities And Exchange Commission of an Exchange Traded Fund, more often abbreviated to ETF… As per Wikipedia, “An exchange-traded fund (ETF) is an investment fund traded on stock exchanges, much like stocks.[1][2] An ETF holds assets such as stocks, commodities, or bonds and generally operates with an arbitrage mechanism designed to keep it trading close to its net asset value,[3] although deviations can occasionally occur. Most ETFs track an index, such as a stock index or bond index. ETFs may be attractive as investments because of their low costs, tax efficiency, and stock-like features.”

So an ETF is one more way of enshrining for Bitcoin an easy method of exposure to mainstream retail and institutional investors, and fully regulated again making them far more desirable and investable than unregulated vehicles… The most prominent current example that would serve as a prototype for a Bitcoin ETF is Grayscale Bitcoin Trust (ticker GBTC) and offers either a Bitcoin trust or a more diversified portfolio consisting of other shitcoins and has been trading since 2013, however it still hasn’t been approved by the SEC and has joined Gemini, VanEck and CBOE on the pending list, as we see with Bakkt the regulators are still cautious no doubt in line with lobbyists and Wall Street power brokers in general… 2018 proved to be a failure for a Bitcoin ETF, and this may well be the case for 2019 as well (although others disagree), however as I constantly re-iterate a financial crisis will likely catalyze the urgency for ETF’s as retail and institutions are forced into alternative currencies and commodities…

The major difference I see when discussing Exchange Traded Funds versus Futures is that unlike purely cash settled futures it is unlikely in my opinion that any Bitcoin ETF can survive in the short or long term without some underlying ownership of bitcoins, in other words it is perfectly possible for an ETF to be fractionally backed by bitcoin but by necessity there must be something to back it, therefore ETF’s will have to purchase underlying bitcoins and store them as the reserve asset for the fund and unlike Futures requires buying reserves and taking bitcoins out of active circulation, i.e hoarding them as the collateral of the fund… Now this fund may be fractionally reserved as many ETF funds are, but in the event of a loss of faith in many of today’s biggest ETF a run on these funds could expose the emperor swimming naked, for you only have a derivative claim on the underlying value which may or may not actually be there… It is highly unlikely in my opinion that any Bitcoin ETF could operate without any underlying bitcoin and with the first Bitcoin ETF likely opening the flood doors to a slew of further Bitcoin ETF’s, there will develop a competition for capital that will be dependent upon the collateral ratio of the ETF, if it is fully reserved then it should be far more likely to attract capital desiring an exposure to Bitcoin, while a low collateral ratio ETF should be attracting less capital, thus hopefully driving a virtuous circle of more fully collateralized funds and less fractionally reserved funds… In any case all these Bitcoin ETF’s if and when they are finally approved by Wall Street’s regulators will unleash a feeding frenzy on fresh supplies of bitcoin, that is currently issued at 12.5 every ten minutes, 75 bitcoins per hour totalling 1800 bitcoins issued daily and trading roughly at $4000 today that is $7,200,000 or seven million two hundred thousand dollars in daily liquidity, a few billion dollars of bitcoins locked up in ETF funds would hoover up a month or a few months worth of fresh supply that would inevitably start driving up the price… It is quite possible that the current twelve months brutal bear market is pierced by and that precipitates the next epic bull run, will be ETF approval for a Bitcoin fund, or many Bitcoin funds…

In conclusion, derivatives unlike Bitcoin exchanges do not allow ownership of actual bitcoins but instead allow the ownership of a derivative with exposure to Bitcoin’s underlying value, and like Bitcoin exchanges have utility and value for both retail and institutional investors… Cash settled Bitcoin futures are valuable for Bitcoin industries such as miners to minimise volatility by hedging a few months forward in the stability of fiat money, while ETF’s are valuable as they have the actual underlying bitcoin locked up as collateral, and while these derivatives cannot and should not be confused with ownership of the underlying asset, the popularity of Futures and ETF’s are in nearly every commodity already and so I expect Bitcoin to be just one more commodity to financialise in Wall Street’s Casinos… And while I predict that Bitcoin is destined to become just another financialised commodity in the near to medium future time horizon, on the long term horizon and as fiat currencies worldwide implode I believe the value of derivatives will wane and the value of the underlying bitcoin will wax… As the trust and value of fiat slowly blows up and evaporates I expect Futures and ETF’s to start blowing up, because why would you want exposure to a derivative when you can own the real thing? As Bitcoin sucks the legacy fiat system of its wealth its derivative structure will suffer first as the feeding frenzy would move to the underlying exchanges and first counter-party ownership of Bitcoin (custodial solutions), however if there were further issues of trust with these custodians, in other words were one or more of these exchanges to be running fractional reserves, then under a run on an exchange would have to limit withdrawals which would only hasten its demise, but even a run on exchanges can be avoided by owning bitcoin in offline cold storage directly under self custody… The safest method of Bitcoin ownership in the long run, (and after many derivatives and rehypothecatory exchange blowups) is not delegating your responsibility over Bitcoin ownership to a third party or custodian but to hold self custody, which necessarily renders redundant and therefore mute derivatives industries… The journey of the average retail and institutional investor may well begin with derivatives exposure, but will ultimately end with direct ownership of Bitcoin, the speed of the journey depends upon the speed of the meltdown of Wall Street and regulatory enforcement…

Exchange Prototype 5: Banking Protocols (FinTech)

The next and in my opinion very important exchange prototype to discuss is not an exchange per say, but I will call them ecosystems or networks that allow fiat money to interact with Bitcoin… These banking protocols are sovereign ledgers and currencies of themselves, but are designed (as far as I can grasp) to streamline and compete with inter-bank exchange, be it SWIFT payments, wire transfers, or international and inter-continental remittances… I do not see these protocols as blockchains such as Bitcoin but unlike most of what you could call “Bitcoin Maximalists” I don’t dismiss these as outright scams but as weaponizing exchange between fiat money and Bitcoin…

While there are a few of these fintech protocols and currencies out there including Stellar Lumens, I will concentrate on the most mainstream currently which is Ripple or XRP and which I discussed in my June 2017 post as a trojan horse for Bitcoin, in that Ripple acts as a convenient and pretty frictionless intermediary step between fiat ownership and bitcoin ownership… Ripple pitches itself as a crypto-currency for retail investors but also pitches itself as an inter-bank protocol, and this is where I find it most interesting… Ripple has been around since 2012 and has sought to integrate with the banking system in a similar manner to SWIFT, with gateways or connections to the banking system while simultaneously being convertible into Bitcoin on any crypto-currency exchange that lists both XRP and Bitcoin… There is no real way to prohibit exchange between crypto-currencies but there is certainly a way to prohibit Ripple from working with the banking system, which brings us to the drawback or weakness of these fintech protocols and that is again banking and securities regulation…

To clear up some possible misconceptions for Bitcoin Maximalists and Ripple Maximalists alike, I doubt that Ripple will ever become a commodity like Bitcoin (and regulated by The CFTC), but is without a doubt in my mind akin to a security and thus under purview of the regulation by the SEC, and therefore its future is far more precarious than Bitcoin’s… Ripple may boast that it is a decentralized protocol and while it may have many thousands or hundreds of thousands of users, its protocol as far as I can see is not really blockchain based (a distributed ledger and consensus system) but a centralized database with a top down developer structure and with the vast amount of currency in the hands of a few of the early founders, at first glance Ripple looks like your classic pre-mined pump and dump exit scam and despite all the Ripple marketing and Ben Bernanke compliments, Ripple could find itself shut down, developers incarcerated, and the project and the future in tatters… Ripple is as centralized and fragile a currency and ledger database as you can imagine and so I do not consider it useful or valuable in the long term, but the short and medium terms are entirely different propositions for these banking protocols…

To take the other side of the debate, Ripple has lobbied the SEC hard, it is one of the oldest crypto-currencies (now seven years old) and has courted interest from numerous banks, and so Ripple seems to be ingratiating itself with the banking system that holds its ultimate fate in its hands, if enough banks deem that Ripple gives increased streamlining in inter-bank exchange operations, overseas payments and remittances markets, then banks would be willing to convert some of their TRILLIONS in bank deposits into XRP would send Ripple’s market cap and currency value into the TRILLIONS… If Ripple gets fully embraced by the banking and securities regulators (in a way by the way Bitcoin can never be embraced) then Ripple could dwarf Bitcoin in value over the short and medium term exactly because it is so more closely connected with the banks… However as I have also discussed the fiat system has long term terminal cancer and that in the long run Bitcoin will de-throne it as the currency of the masses, the slow and medium term bleed of value is from fiat into Bitcoin and with it in my opinion will come Ripple and XRP as transitionary layers… While Ripple itself is at essence one large fiat to Bitcoin exchange and gateway and is inherently centralized and fragile, in reality it is more of a network of exchanges that could encompass retail investors and traders, banks, wire transfer providers, automatic clearing houses and institutional investors, and so is far more decentralised and anti-fragile an exchange layer than conventional centralised exchanges… I also imagine that because of XRP and a sovereign currency (that further differentiates itself from centralized exchanges) that KYC/AML regulations would be far more difficult to track and enforce through Ripple with hundreds or thousands of gateways compared to the one gateway of a traditional exchange… In that way Ripple may prove to be a major headache for regulators and banks trying to keep a track on capital flows compared to single exchanges, and so bankers and regulators may actually have a bigger incentive to clamp down or dismantle Ripple rather than work with it if they deem it a threat to their control and stability, but also Ripple would likely weaponize banking fees compared to single exchanges… In every way banking protocols and fintech in general are double edged swords for the bankers that will ultimately control and regulate them… This is a very interesting space to continue monitoring…

Exchange Prototype 6: Stablecoins

The last major prototype to discuss are stable coins, and these are again creations that trigger and offend many within Bitcoin and many more without, they are scamcoins of scam exchanges and have no value whatsoever, are ponzi schemes created by fraudulent exchanges to enrich themselves, and so on… The most notorious of the past few years has obviously been Tether as really the first prototype of what will in my opinion become a development on every major exchange and what is essentially just double-entry book-keeping, taking in fiat deposits of dollars, pounds, euros, yen on the debit side of the ledger, and issuing the corresponding currency on the credit side of the ledger… This may not sound much at first thought but it’s an interesting work around for the obvious limitations of fiat currencies and KYC/AML regulations, by essentially converting fiat deposits in dollars into Tether (Tether’s Unit USDT, pegged to the dollar) the limitations of KYC/AML are transferred to the issuer (Bitfinex) but the currency can basically travel anywhere… This means that if other exchanges list and accept Tether as an exchange currency, what is essentially fiat money can travel to places that fiat could never reach, and it makes feasible exchanges that only deal in crypto-currencies and can therefore evade KYC/AML regulations (at least for now) far easier than if they had to deal with banks directly…

In essence a stablecoin allows one exchange to become a hub for issuing credit to other exchanges, and can develop a web of capital flows which has no doubt been picked up by select Twitter accounts with a desperate obsession, and which does throw up more than one question about the operations at Bitfinex, and they have not really helped themselves in this regard… Having suspended exchanging for US customers (flouting the SEC) and being based out of a secretive tax haven, there is a fair chance that Bitfinex has recycled dirty money, and because of this lack of regulation (thus far) accountants have been unable or unwilling to sign official and recognized audits, and so naturally the conspiracy theories have been rampaging as to what exactly is going on between Bitfinex and their spawn in Tether… While Bitfinex may be holding fractional reserves and printing more Tether than they have fiat currencies deposited there is another explanation why they cannot get accountants to sign off on any audits, and that would be the banks on the other side of the ledger… It is these banks that are the first line of enquiry for regulators and KYC/AML compliance, and therefore it would be the secrecy and possible nefarious dealings of the servicing banks that forbid any official audit in case their assets at Bitfinex come to the light, which brings us back yet again to this question of regulation… The first generation of exchanges (which includes Bitfinex) came of age before any real national or international regulation of crypto-currency and therefore have been largely able to skirt securities and commodities regulators, and because Tether is a stablecoin issued by a largely unregulated exchange then it stands to reason that Tether is a largely unregulated stablecoin, but as regulations develop I expect the next generation of stablecoins that get approved by Securities Regulators to be fully audited and the exchange workings to be transparent, exactly in order to satisfy the regulators and thus get issued licences and access to the banking system… These fully regulated and liquid exchanges and stablecoins I believe will chip away at Bitfinex and Tether, and as these grow so the influence of Tether on the short term liquidity at Bitcoin exchanges will wane, much to Bitfinexed chagrin Tether may just go out with a whimper than a bang…

The other major advantage of stablecoins for traders is the hedging of crypto-currency volatility with the stability of fiat currency… As stablecoins are by design and definition a claim upon fiat currency and with the vast amount of current stablecoins pegged to the dollar, traders can exit stablecoins during crypto-currency bull markets and can either book profits or mitigate losses by flooding back into stablecoins and dollar backed stability during crypto-currency bear markets… Therefore over the short to medium term and with the fallback option of stability coins, liquidity does not have to flow back into the fiat currency system but can be stored offshore so to speak still within the crypto-currency ecosystem, but denominated in dollars… A hybrid holding that spans a legal gray area, but again dependent upon the issuer and exchange…

For examples of new generation stable coins, see Goldman Sachs based Circle’s USDC, and just in last two weeks, to much fanfare and much mocking over social media, Jamie Dimon and J P Morgan’s JPMCoin… The Too Big To Fail banks want in!

Exchanges – All Shapes And Sizes

I have provided a highly detailed breakdown of the most popular exchange prototypes and these are far from an exhaustive list, there will be many more I’m sure world wide in the near to medium term time horizon, and are connections or gateways into Bitcoin that cater to both the individual and the institution, they can cater for virtually anonymous and KYC/AML free surveillance of buying and selling through decentralised exchanges and autonomous organisations protecting privacy for a more inconvenient process and with a higher price premium, or they can cater for complete KYC/AML regulation and surveillance with a highly convenient and low price premium for buying and selling Bitcoin, exchanges come in all shapes and sizes with varying degrees of regulation to satisfy the banking system before they open themselves to an entirely new frontier of digital assets… While the mere thought of regulation and compliance are complete anathema to libertarian oriented Bitcoiners who only envisage a Bitcoin free of regulation, the reality is that the wealth is currently trapped in the fiat currency debt ponzi scheme and that to travel into Bitcoin at more than the minor trickle of the last ten years, and for the convenience and security for most of the investing public and critically for institutional investment, will require Know Your Customer and Anti Money Laundering regulation for any centralised exchanges in a far more pervasive way than up until now, the first decade of Bitcoin exchanges was largely unregulated, outside of decentralised exchange and evasion of KYC/AML future exchanges will undoubtedly be regulated as a foundering banking system and highly levered derivative financial system will be desperate to flood into, that cash apps, centralised exchanges, derivative exchanges, fintech protocols and stablecoins will all contribute to…

Even though I have spent the last eleven thousand words explaining past current and future exchanges is as much generic detail as I can, I need to discuss a far larger context and the last ten years of Bitcoin before this recent development of regulated exchanges… Critical to this discussion is where we are in the currency issue schedule of Bitcoin, which opens up a completely new dimension of further discussion…

Bitcoin Issue Schedule And Current Status

The above chart is critical to read and to appreciate as it puts into context all of the above discussion regarding exchanges (issue rate in blue, inflation rate in orange)

On January 3rd 2009 Bitcoin was launched with a block reward of fifty bitcoins every ten minutes, and this lasted until November 28th 2012 when the first 210,000 blocks had been mined, thus in the first four years of Bitcoin (210,000 x 10 minutes) half of Bitcoin’s maximum cap of Twenty One Million (21,000,000) was issued, or 10,500,000 (210,000 x 50)… It was at this point that an intrinsic feature of Bitcoin was triggered, and that is the phenomenon of a block reward halvening, or otherwise stated the issue of bitcoins dropped from 50 every 10 minutes to 25 every ten minutes…

From November 2012 to 9th July 2016 Bitcoin mined another 210,000 blocks with a block reward of 25 bitcoins every 10 minutes and a total issue of 5,250,000, for a cumulative total of 15,750,000 btc mined in eight years, out of 21,000,000… As I discussed at length in my Bitcoin Halving post of 2016, Bitcoin underwent another block reward halvening from 25 bitcoins every ten minutes to 12.5 bitcoins every ten minutes, that will last until May 2020 when there is another currency halvening…

Sometime around the 24th of May next year (2020) Bitcoin will again reduce the block reward by half, and between 2016 and then another 2,625,000 bitcoin will have been mined for a cumulative total of 18,375,000, again out of a maximum cap of 21,000,000…

What tortured point am I trying to make? The simple point I am making is that for all the talk of exchange and exchanges in this post, and all the pent up demand that I believe is sure to come from banks and legacy institutions drowning in their own insolvency, they will all be competing for less than 3 million bitcoins in newly mined currency for the next one hundred and twenty years, and for the 1,312,500 bitcoins issued between 2020 and 2024 at 900 per day… What should be clear is that newly issued bitcoins pale into insignificance compared to the Eighteen Millions bitcoin already issued over the last decade (and before Wall Street got anywhere close to it), and so we need to discuss further the last ten years and existing bitcoin ownership…

The Bitcoin Hodlers – Drivers Of The Future

Of the approximately 17,500,000 bitcoins mined so far it is a fair estimate in my opinion that at least 5,000,000 are lost forever, as in the early years the lack of infrastructure and convenient storage solutions meant that many of the early coins were mistakenly destroyed, more than likely because of the simple forgetting of a password, so I think it would be fair to estimate that around 12,500,000 remain, distributed between all Bitcoin users, which could be miners (as issuers) and users (as recipients)… It should be clear that these Hodlers will hold far more of an influence on the development of Bitcoin than those who issue and consume the remaining 3,000,000, because they and only they will decide what they do with the bitcoins they are already sitting on…

The first question is why are they still Hodling? The rather simple answer is that they are still betting on it going up in the future and being supported by a new inflow of capital and wealth seeking ownership of what they already have… In the next financial crisis and stock and bond bear markets that will pressure individuals, banks and institutions to seek safety in the security and scarcity of Bitcoin, will likely unleash another bull market in the currency as a flood of demand will hit a limited supply that is currently 1,800 per day (daily liquidity at a laughable $7,200,000 with Bitcoin price at $4,000), and from May 2020 drops to 900 per day (daily liquidity at $3,600,000 with Bitcoin price at $4,000)… This bull market that will probably make the Bull Market of 2017 look rather insignificant in the big scale of things, will lead to the soaring wealth of Bitcoin Hodlers and a far higher price and value for the asset that they already own, which also brings forward the day that they decide to consume or sell some or all of their bitcoins, all this naturally dependent upon individual time preference and compunction to consume…

If Hodlers decide to consume (i.e sell) their bitcoins there are realistically two options: the first option is to exchange for fiat currency and on an exchange, centralised or decentralised, with or without KYC/AML and therefore a possible taxation shakedown, the second option is to sell bitcoin for goods and services or alternatively stated peer to peer barter with someone who accepts bitcoin for their goods or services… The first option requires further interaction with the fiat system and the capital controls, regulation and taxation and the second option does not, and this choice may not be a binary one but a balance of both, for at least for now most if not all Hodlers still have a foot in the legacy fiat system, they are paid in fiat currency, they can mostly only consume in fiat currency, they have debt denominated in fiat currency and so on… The more the price of Bitcoin falls the more Hodlers are sucked back into the legacy fiat system for survival while the higher the price of Bitcoin goes the more the Holder is freed from the fiat legacy system, the more Bitcoin falls the less incentive new Holders have to accept Bitcoin the more Bitcoin increases in value the more the incentive for new Holders to accept, so the Bitcoin price is critical and central to Bitcoin adoption…

If you accept that Bitcoin will go more up than down over time then it should also become clear that the incentive for the Hodler is to move away from fiat as much as possible (paying down debt is the obvious first step), and wait for new adopters who will accept your bitcoin directly and therefore with no taxable event or KYC/AML event, all this dependent on time… And this brings us to the main drawback of Bitcoin as a means of exchange for peer to peer barter, that while it is a decentralised and anti-fragile anti-correlated digital asset for store of value purposes, the same scarcity of block space and capacity makes it a pretty terrible medium of exchange and payment system, far inferior to the current fiat payments system that is itself a horrendous store of value and why Bitcoin exists… Bitcoin can never scale as a payments system on its native blockchain that is geared toward security, is far from anonymous, and is costly and slow to transact upon, so Bitcoin cannot ever become a convenient medium of exchange in its current form, which inhibits consumer and merchant adoption that keeps fiat exchanges relevant and still useful, at least until now…

Bitcoin And Second Layer Effects – Lightning Network And Payment Processing

2017 was a watershed year for the Bitcoin Protocol, we had the Scaling Debate, UASF Game Theory, and finally SegWit Activation which provided a capacity upgrade alongside a transaction malleability fix, which for the first time made it feasible to develop smart contract functionality for off chain payment layers… By leveraging Bitcoin’s underlying immutable security for smart contract layers, the old achilles’ heels of transparency, slowness and costliness of Bitcoin transactions is transformed into full anonymity, lightning speed and virtually zero cost transactions which makes the entire concept of micro payments for the first time feasible… Bitcoin is being your own bank, whereas the Lightning Network is being your own payment processor…